Argan, Inc. catches your eye-a construction powerhouse riding the AI and renewable energy wave with a $1.9 billion backlog and zero debt. Whether you’re a retail investor chasing growth or an institutional player seeking diversification, Argan’s blend of explosive earnings and cyclical exposure demands your attention. Here’s why this stock could be your next big win-or a cautionary tale.

Argan Inc. operates through its wholly-owned subsidiaries, Gemma Power Systems (GPS) and Southern Maryland Cable (SMC). GPS provides a range of services to the power generation and renewable energy markets, including development, consulting, engineering, procurement, construction, commissioning, operations, and maintenance. SMC offers telecommunications infrastructure services, including project management, construction, and maintenance.

Argan, Inc. is a construction powerhouse, delivering engineering, procurement, and construction (EPC) services through subsidiaries like Gemma Power Systems and Atlantic Projects Company. Its core focus is the power generation market, building renewable energy facilities (biomass, wind, solar, battery storage) and natural gas plants across the U.S., Ireland, and the U.K.

The company also offers industrial and telecom infrastructure services, catering to utilities, independent power producers, and government clients. With a record $1.9 billion project backlog, Argan is riding the wave of electrification and AI-driven energy demand.

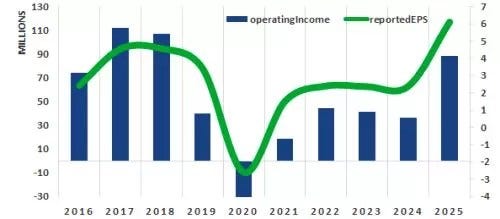

Argan’s fiscal 2025 was a breakout year, with revenues soaring 53% to $874.2 million and net income skyrocketing 164% to $85.5 million. In Q1 FY2026, revenues grew 23% year-over-year to $193.7 million, with EPS of $1.60 crushing estimates of $0.90. The company boasts a pristine balance sheet with $546.5 million in cash, zero debt, and a 19% gross margin, signaling robust operational efficiency. These metrics highlight Argan’s ability to deliver consistent profitability in a high-demand market.

Argan’s price-to-earnings ( P/E) ratio of 31.1x is slightly below the construction industry average of 34.5x, suggesting a relatively attractive valuation. Its price-to-book (P/B) ratio of ~4.5 and return on equity (ROE) of ~15% reflect solid value creation.

The company’s Operating margin of 11.8% and EBITDA of $69.5 million underscore its efficiency and cash flow generation. These ratios make Argan a compelling pick for value-conscious investors.

Argan’s stock (NYSE: AGX) has surged 46.7% year-to-date as of September 2025, hitting an all-time high of $253. Over the past five years, it’s delivered a staggering 233.9% return, outpacing many peers. However, recent Q2 results saw a 7% dip to $222 after EPS of $2.50 beat estimates but showed a quarterly decline.

Analysts remain bullish, with a “Buy” rating and a $202 price target, signaling confidence despite short-term volatility.

The stock price has risen by more than 1 089% since the IPO.

Argan competes with firms like Quanta Services, EMCOR Group, and Sterling Infrastructure in the power and construction sectors. Its niche in renewable and gas-fired power plants, coupled with a debt-free balance sheet, gives it an edge. The company’s record backlog and focus on high-demand sectors like AI data centers and EV charging infrastructure position it to capture market share. However, tariffs and supply chain risks could challenge project timelines.

Competitor Comparison Table:

Data as of September 5, 2025, sourced from Yahoo Finance and other public sources.

Since our last analysis, Argan, Inc.’s Investment Scoreboard rating has dipped slightly from 68 to 65. This modest decline is hardly a red flag for a company with virtually no debt and a fortress-like balance sheet. While Argan’s stellar profitability in fiscal 2025-highlighted by a 164% net income surge-paints a rosy picture, investors should note its cyclical nature.

The company’s performance is closely tied to financial market conditions and macroeconomic trends, such as the U.S. housing starts decline since April 2022, which could signal headwinds for construction-related firms.

Argan’s operational strength, driven by a $1.9 billion project backlog and expertise in power generation, makes it well-equipped to weather market turbulence. Its debt-free status and $546.5 million cash reserve provide a buffer against economic downturns. This resilience positions Argan as a reliable portfolio diversifier, particularly for investors seeking exposure to energy infrastructure.

For savvy investors, Argan is a tactical holding: overweight it early in the economic cycle to capture growth, then trim exposure as the cycle peaks. The company’s focus on high-demand sectors like AI data centers and renewable energy aligns with long-term trends, enhancing its appeal. However, at current valuations, with a P/E ratio of 31.1x and a recent stock price of $222, we believe the market may be pricing in overly optimistic growth expectations.

Argan remains a compelling pick for diversification, but caution is warranted. Its cyclical exposure and sensitivity to macroeconomic shifts, like declining construction activity, suggest potential volatility. We recommend holding Argan for its defensive qualities but advise monitoring market conditions closely. At present, the stock appears overvalued, so investors may benefit from waiting for a better entry point.

2025–2029 Price Targets:

It’s evident that the stock price is near its All-Time High (ATH). Additionally, the market has begun to correct itself-great news! We’re patiently waiting for an even deeper correction before making our move to buy.

Argan pays a quarterly dividend of $0.375 per share, yielding 0.73% annually, with a 50% increase over two years. Its share repurchase program was recently expanded to $150 million, reflecting confidence in long-term value. The company has returned over $217 million to shareholders since 2011. This disciplined approach balances growth investment with rewarding investors.

Argan recently secured a major contract for a 1.2 GW natural gas-fired power plant in Texas, pushing its backlog toward $2 billion. Q1 FY2026 results showed strong revenue and EPS growth, driven by power sector demand from AI and EV markets.

The appointment of energy veteran Lisa Larroque Alexander to the board adds strategic heft. These developments signal sustained growth, though a recent 7% stock dip post-Q2 reflects cautious trader sentiment.

The record backlog and new contracts enhance Argan’s revenue visibility, boosting its intrinsic value. Strong financials and zero debt provide resilience against market volatility, making it attractive for long-term investors. However, high implied volatility and potential tariff risks could temper short-term gains. Analysts see a 10–15% upside, supported by secular energy trends.

Note: X posts reflect sentiment and are not conclusive evidence.

Argan, Inc. is a dynamo in the energy infrastructure space, blending explosive growth with a rock-solid balance sheet. But with its stock near all-time highs and a correction looming, don’t chase it like a kid after an ice cream truck-wait for a dip to scoop up value. This cyclical star shines brightest for patient investors who time the market’s rhythm. Keep your eyes on the prize and your wallet ready for the right moment.

Or Donate:

*Investment analysis involves scrutinizing over 50 different criteria to assess a company's ability to generate shareholder value. This comprehensive approach includes tracking revenue, profit, equity dynamics, dividend payments, cash flow, debt and financial management, stock price trends, bankruptcy risk, F-Score, and more. These metrics are consolidated into a straightforward Investment Scoreboard, which effectively helps predict future stock price movements.

**Use the price forecast to manage the risk of your investments.

Originally published at https://www.aipt.lt on September 5, 2025.

Unlock Argan Inc.’s Secrets: Is This Stock Your Next Big Win? was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.