Bitcoin is trading just above $60,000 right now, and the network's estimated all-in cost to produce a single coin is near $84,300, so the gap between the two is roughly a quarter, leaving mining underwater on a full-cost basis across much of the network.

For years, the assumption was that this simply couldn't happen, that production cost set a hard floor under the price, the thinking being that Bitcoin miners would switch off and the market would catch itself well before Bitcoin price fell that far below what it costs to make a coin. And yet the price has now spent weeks under that line, and the network is still running fine.

What gave way in mid-June is a good illustration of how the correction works in practice. Difficulty fell 10.09%, dropping from 138.96 trillion to 124.93 trillion, which Galaxy Research clocked as the second-largest downward adjustment of 2026 and the eleventh-largest in the network's entire history.

That epoch ended up running 15.6 days against a 14-day target because so many higher-cost machines had gone dark once their margins disappeared. The protocol noticed the slower blocks and lowered the bar for everyone still hashing, so the self-correcting mechanism people like to invoke is real, and it does work, just not in the way the floor argument tends to assume.

All of this comes down to hashprice, the daily revenue a Bitcoin miner earns per unit of computing power. Hashprice falls when BTC falls, network difficulty climbs, or transaction fees thin out, and it rises when BTC rallies, fees spike, or enough weak miners leave that difficulty resets to a lower level for whoever survives.

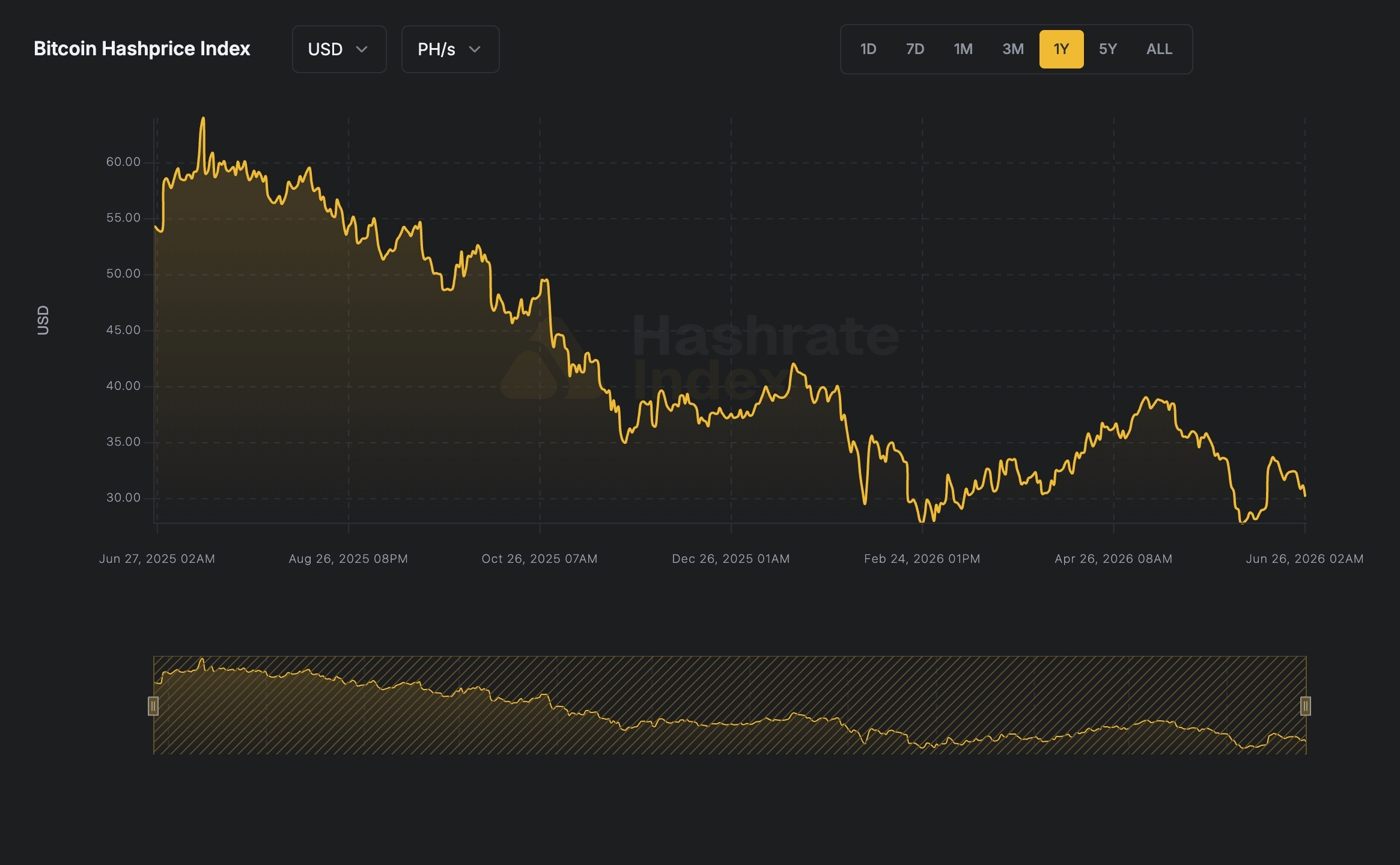

To put that in context, hashprice peaked near $63 per petahash per day back in July 2025, then sank into the high $20s by early June, a level that Hashrate Index and most operators treat as gross breakeven before you even get to debt and overhead, and it has since clawed its way back above $30 in the wake of the June difficulty cut.

In its Q1 2026 mining report, CoinShares put the weighted average cash cost to produce one Bitcoin among public miners at roughly $79,995 in the fourth quarter of 2025, with hashprice sliding from the $36 to $38 range down toward $29. It estimated that somewhere between 15% and 20% of the global fleet will end up underwater once power costs run high enough.

The thing those averages hide, though, is the enormous dispersion across operators, which is the whole reason production cost can't function as a floor. A Bitcoin miner running the latest-generation hardware below 15 joules per terahash on sub-5-cent power keeps a healthy margin in the same market where an older fleet paying 6 or 7 cents is bleeding cash on every block it finds.

When Bitcoin's price drops, revenue per unit of hash drops right along with it, and the highest-cost machines start being uneconomic, at which point their operators start doing the obvious things: selling BTC, switching off rigs, delaying expansion, renegotiating their power contracts, or raising fresh capital to ride it out.

Once enough hash rate leaves the network, difficulty adjusts lower, and the miners who stayed online get to collect a larger share of the same block subsidy, which relieves the pressure, though it does so slowly and unevenly and does nothing to stop the price from falling while all of that is grinding through.

So production costs end up deciding who can keep producing as Bitcoin slides, but they've never been the thing that decides where the slide actually stops.

In earlier downturns, a stressed miner really had only two options: keep hashing or power down. But the largest public operators now have a third option: to turn the company into an AI and high-performance computing business.

CoinShares counts more than $70 billion in cumulative AI and HPC contracts announced across the public sector at this point, and it reckons listed miners could be pulling as much as 70% of their revenue from AI by the end of 2026, up from something closer to 30% today.

The scale of the individual deals points the same way, with Core Scientific's expanded arrangement with CoreWeave alone running to $10.2 billion over twelve years, TeraWulf having booked $12.8 billion in contracted HPC revenue, and Hut 8 signing a $7 billion, fifteen-year lease for AI infrastructure, while Bitfarms has gone so far as to drop Bitcoin from its name entirely.

This is splitting the sector into three camps. A handful of miners have signed AI contracts and are already moving capacity and funding the shift with debt, the best example being Cipher, whose $1.7 billion in senior secured notes pushed a single quarter's interest expense to $33.4 million.

A second group is sitting on frameworks and early pilots that haven't yet turned into revenue, and a third is still tied almost entirely to Bitcoin and therefore exposed to every move in hashprice.

That divergence is starting to show up in how the market values these companies, since the hybrid infrastructure names now trade partly on contract delivery and execution risk, while the pure-play miners trade as a much cleaner bet on BTC, difficulty, and treasury policy. And then the low-cost niche operators sit apart from all of them, small and flexible enough to benefit on the occasions when difficulty resets, and cheap power frees up.

Public Bitcoin miners have reduced their holdings by more than 15,000 BTC from peak levels, with Core Scientific offloading about 1,900 coins in January and planning to clear most of what remains, Bitdeer cutting its balance to zero in February, and Riot selling 1,818 coins back in December.

To put that speed in perspective, the first quarter of 2026 alone saw public miners shed more BTC than they did across the whole of 2025, a pace of treasury liquidation that surpassed even the dumping the market saw during the Terra-Luna collapse.

If Bitcoin recovers toward $100,000, then hashprice eases back toward $37, treasury sales slow down, and hardware refresh cycles resume.

If it chops sideways near its cost of production, the sector grinds, with public miners selling coins and chasing AI deals while difficulty does some of the repair work for them.

And if it falls further, higher-cost hash rate keeps going offline, the equity gap between the hybrid and pure-play names widens, and the operators sitting on the cheapest power pick up share.

The important thing is that none of those paths breaks the network, which is the part the bear case tends to oversell. You can already see it in the way the mid-June drop has partly reversed, with block times back near 10 minutes and some of the curtailed capacity returning as the price steadied, all of which suggests the hash rate that left was reacting to thin margins more than abandoning the network.

The pivot to AI carries its own risks for network security, of course, and a cooling AI cycle would hit the hybrids before Bitcoin itself saw any relief, so the best signals to keep an eye on from here are hashprice, the cadence of the difficulty adjustments, public-miner treasury balances, and the coins those miners are sending off to exchanges.

The point that survives all of this is the one the floor argument keeps getting wrong: that Bitcoin can trade well below what it costs the average Bitcoin miner to produce a coin. It can stay there for a while, because the cost of production sorts producers; it was never going to support the price.

And the longer BTC spends below that level, the more sharply the network gets divided along it, separating the operators who own cheap power and modern machines and a credible second business from those who have simply run out of ways to wait.

The post Bitcoin’s broken production cost floor is splitting miners into survivors and sellers appeared first on CryptoSlate.