Craving a hot investment opportunity? Lamb Weston Holdings, Inc., the global titan of frozen fries, is sizzling at a five-year low, poised for a breakout. With a juicy 3.01% dividend yield, activist-driven restructuring, and a stock price showing signs of a bullish reversal, now’s the time to dig into this undervalued gem. Here’s why institutional and retail investors are eyeing Lamb Weston for portfolio gains in 2025 and beyond.

Lamb Weston Holdings is North America’s largest and the world’s second-largest producer of frozen potato products, from classic French fries to sweet potato fries, tater tots, and hash browns. Headquartered in Eagle, Idaho, the company operates through three key segments:

With 10,700 employees and a sprawling network of production facilities, Lamb Weston delivers to over 100 countries, with McDonald’s alone accounting for 14% of its 2024 sales. Its manufacturing blends traditional expertise with cutting-edge tech, ensuring consistent quality and a robust supply chain that keeps the fries flowing.

What makes Lamb Weston stand out? Its ability to innovate-think new fry cuts or healthier options-and its deep partnerships with major clients like fast-food chains and grocery stores. This isn’t just a potato company; it’s a supply chain powerhouse that thrives on efficiency and customer trust.

Lamb Weston’s financials tell a story of resilience amid challenges. In its Q4 FY2025 earnings (reported July 23, 2025), the company posted a 4% revenue increase to $1.68 billion, beating estimates of $1.59 billion, driven by contract wins and a 15% surge in international sales.

Adjusted EPS of $0.87 also topped expectations of $0.63, signaling a return to growth momentum after a tough year. However, the trailing twelve months (TTM) show a Net loss of $36.1 million and a negative EPS of -$0.25, reflecting margin pressures from higher manufacturing costs and softer quick-service restaurant (QSR) traffic.

While FY2025 was rocky with a 25% drop in Adjusted EBITDA to $282 million, Lamb Weston’s updated FY2026 outlook projects net sales of $6.35-$6.55 billion and Adjusted EBITDA of $1-$1.2 billion, reflecting confidence in recovery through cost-cutting and strategic realignment.

Lamb Weston’s stock (NYSE: LW) has had a volatile year. As of June 3, 2025, it traded at $55.75, up from a 52-week low of $47.90 but down 11.83% over the past year, underperforming the S&P 500. A 20% surge followed its strong Q4 FY2025 results, driven by better-than-expected earnings and a new restructuring plan.

However, the stock remains well below its 52-week high of $88.25, reflecting investor concerns about prior guidance cuts and operational hiccups, like the botched ERP system rollout in 2024 that dented market share.

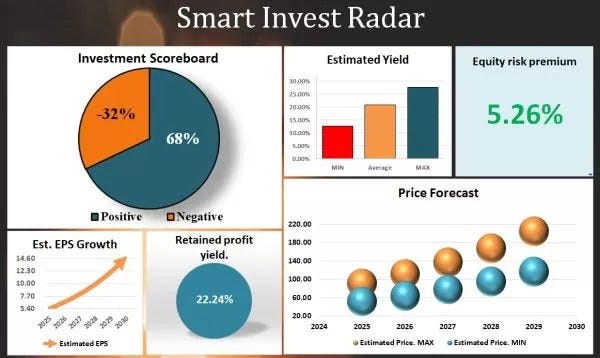

Analysts rate LW a “Buy” with an average price target of $78.22, suggesting modest upside, and some see it as undervalued with a “Real Value” estimate of $91.82.

The stock price has risen by more than 67.12% since the IPO.

Lamb Weston operates in a competitive frozen food market, facing off against giants like Kellanova, Treehouse Foods, Pilgrim’s Pride, Campbell’s, and Hormel Foods, as well as private-label producers. Its edge lies in its scale, innovation, and long-term partnerships with major QSR chains like McDonald’s.

However, private-label brands and rising input costs pose threats, especially in a price-sensitive market. The company’s recent move to cut North American potato processing capacity to the low- to mid-90% utilization rate aims to align supply with demand, potentially boosting pricing power and margins. This strategic shift helps Lamb Weston stay competitive despite soft QSR traffic and inflationary pressures.

Our analysis reveals that Lamb Weston Holdings, Inc. is a robust company with significant growth potential, making it an attractive option for portfolio diversification and steady dividend income. Operating in a highly competitive environment, the company faces challenges that have kept profitability metrics modest. For instance, its gross margin reached 27.32% in 2024, marking a historical high but still reflecting the pressures of a tough market.

However, if Lamb Weston successfully addresses its operational hurdles and executes its strategic goals (detailed below), it could emerge as a standout performer for investors. Under favorable market conditions, our projections suggest the company’s stock price could grow at an average annual rate exceeding 11%, significantly outpacing its historical 10-year compounded annual growth rate (CAGR) of 3.57%. This combination of resilience, dividend reliability, and upside potential positions Lamb Weston as a compelling choice for both institutional and retail investors seeking value and income in a dynamic market.

2025–2029 Price Targets:

The company’s stock price is currently rebounding from a five-year low, forming a strong support level. This presents a highly favorable opportunity for investors to buy shares or increase their existing position in the market.

Moving Averages (MA):

Relative Strength Index (RSI):

Moving Average Convergence Divergence (MACD):

Volume Trends:

Price Patterns:

Lamb Weston is committed to returning value to shareholders. Its dividend yield stands at 3.01%, with an annual payout of $1.48 per share (quarterly dividend of $0.37, next ex-dividend date August 1, 2025). The company has raised its dividend for 7 consecutive years, with a payout ratio of 56.32%, balancing shareholder returns with reinvestment.

Additionally, the board approved a $250 million increase in its share repurchase program in FY2025, with $100 million already returned via buybacks in Q3. This shareholder-friendly approach, combined with a 28.57% dividend growth rate, makes LW attractive for income-focused investors.

The big news for Lamb Weston in 2025 is its “Focus to Win” restructuring plan, announced alongside Q4 FY2025 results. This includes a workforce reduction and a $250 million cost-saving target by FY2028, aimed at streamlining operations and boosting profitability. The market cheered, with the stock jumping 20% post-earnings, reflecting optimism about improved margins and efficiency.

However, activist investor JANA Partners, holding a 7% stake, has been shaking things up. In June 2025, JANA pushed for significant board changes and even a potential sale, citing Lamb Weston’s bottom-quartile performance and $400 million in EBITDA losses over 2.5 years.

This led to a board restructuring agreement, adding six new directors and retiring four, signaling a shift toward more aggressive governance and strategy. While this could unlock long-term value through better execution or strategic deals, it also introduces uncertainty, contributing to stock volatility.

On the downside, S&P Global Ratings revised Lamb Weston’s outlook to negative from stable, citing operational challenges, though its strong liquidity and profitability metrics provide a buffer. The company’s focus on cost-cutting and capacity alignment should help stabilize its financials, but weak QSR demand and past execution missteps (like the ERP fiasco) remain risks.

Why Should Investors Care?

For institutional investors, Lamb Weston offers a compelling mix of defensive qualities (food is recession-resistant), a strong dividend, and activist-driven upside potential. Its undervaluation (P/E of 14.19x and “Real Value” of $91.82) and analyst “Buy” rating make it a candidate for value and growth portfolios.

For retail investors, the stock’s 3.01% dividend yield and consistent payout growth are hard to ignore, especially in a volatile market. The restructuring plan and activist pressure signal a company in transition, potentially poised for a comeback if it executes well. However, risks like QSR slowdowns and competitive pricing pressures warrant caution.

Lamb Weston is a savory blend of resilience, income, and growth potential. Trading near a five-year low with strong technical support, its “Focus to Win” restructuring and activist momentum signal a turnaround. While risks like QSR slowdowns linger, the company’s 3.01% dividend, robust buyback program, and projected 11%+ annual stock growth make it a compelling pick for value and income investors. Grab a seat at the table before this stock heats up!

Or Donate:

*Investment analysis involves scrutinizing over 50 different criteria to assess a company's ability to generate shareholder value. This comprehensive approach includes tracking revenue, profit, equity dynamics, dividend payments, cash flow, debt and financial management, stock price trends, bankruptcy risk, F-Score, and more. These metrics are consolidated into a straightforward Investment Scoreboard, which effectively helps predict future stock price movements.

**Use the price forecast to manage the risk of your investments.

Originally published at https://www.aipt.lt on July 24, 2025.

Lamb Weston Holding Is Rebounding: Time to Buy This 3% Dividend Powerhouse? was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.