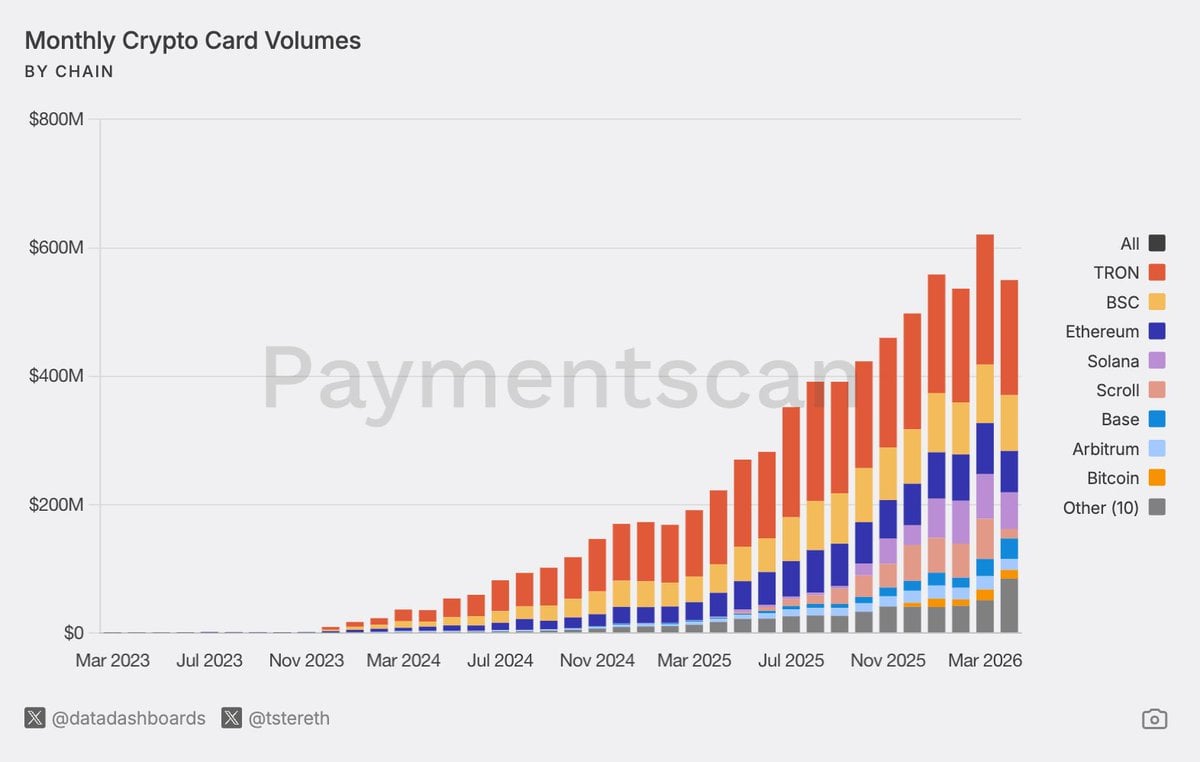

Crypto card spending is breaking out of its early-adopter box, and the numbers are getting too large to ignore. Monthly crypto card volume has surged about 500% since September 2024 to roughly $600 million, turning stablecoin-linked cards into one of the fastest-growing payment stories on public blockchains.

The shift shows stablecoins moving from wallet balances and exchange liquidity into everyday consumer spending. Users are not only holding digital dollars anymore. They are increasingly routing them through card networks, mobile wallets, cashback programs, and merchant payment flows that feel familiar to mainstream users.

Visa is dominating that bridge. Data shared by The Kobeissi Letter and later circulated across market reports placed Visa’s share near 90% of on-chain crypto card transactions, with the network reportedly processing around 97% of crypto card volume in March. That makes Visa the clearest winner in the first major wave of stablecoin card distribution.

Visa has been expanding stablecoin-linked payments from two directions: consumer card access and backend settlement. The company’s stablecoin settlement pilot now supports nine blockchains and has reached a $7 billion annualized run rate, up 50% from the previous quarter.

That matters because the card side and the settlement side reinforce each other. Consumers want the simplicity of tapping a card or using Apple Pay. Issuers and payment companies want faster settlement, programmable liquidity, and fewer frictions than older banking rails. Stablecoins sit in the middle, giving the system dollar-like value that can move across blockchain infrastructure while still connecting to existing merchant networks.

Visa’s Bridge-enabled stablecoin-linked cards are already live in 18 countries, with plans to expand to more than 100 countries across Europe, Asia Pacific, Africa, and the Middle East by the end of the year. The model allows developers and fintechs to issue cards backed by stablecoin balances while merchants receive normal card payments.

That is the real power of the setup. Merchants do not need to understand wallets, gas fees, seed phrases, or stablecoin custody. The user spends crypto, the merchant receives a familiar payment, and the card network keeps the transaction inside a trusted consumer experience.

Stablecoins have already become critical to trading liquidity, collateral movement, and cross-border settlement. The new card surge shows a different kind of adoption: consumer distribution.

That shift lines up with the broader race over who controls stablecoin settlement. Traditional payment companies, crypto infrastructure firms, wallets, exchanges, and fintech apps all want the same prize: the point where a digital-dollar balance becomes spendable in the real world.

Cards are winning the early round because they solve the cold-start problem. Native stablecoin checkout still requires merchants to integrate new rails, manage compliance questions, and handle unfamiliar payment flows. A Visa-linked stablecoin card skips much of that friction by using existing acceptance networks while crypto infrastructure runs behind the scenes.

That makes the current surge less about novelty and more about distribution. Stablecoins may be blockchain assets, but cards give them a route into groceries, travel, subscriptions, restaurants, online shopping, and mobile wallet payments.

Newer crypto-native programs are also pushing the category beyond simple spending. Jupiter’s Solana-based card model has drawn attention for cashback tiers that reportedly return 4% to 10%, with April volume growth placed at 660% month over month.

That type of incentive changes user behavior. Crypto cards become more than a way to cash out into fiat. They become rewards products, loyalty engines, and spending accounts built around stablecoin balances. Instead of airline points or bank rewards, users receive digital-dollar incentives that can stay inside crypto rails.

The cashback race also explains why card spending can grow quickly even before merchants adopt native stablecoin payments. Users already understand rewards. They already understand tapping a card. If a crypto-native product can deliver higher rewards and smoother settlement, the behavioral jump becomes much smaller.

Crypto’s consumer adoption problem has always been usability. Wallets can be powerful, but they are still too complex for many users. Exchanges are familiar to traders, but they do not always feel like spending apps. Native blockchain payments are efficient in theory, but merchant adoption remains uneven.

Stablecoin cards solve that by hiding the complexity. The customer sees a card. The merchant sees a card. The infrastructure underneath handles stablecoin funding, conversion, settlement, and routing.

That is why the $600 million monthly volume figure is important. It suggests crypto payments are not waiting for a perfect native checkout system before reaching consumers. They are moving through the rails people already know.

The risk is that Visa’s early lead could turn stablecoin spending into another layer of card-network dependency rather than a fully open payment revolution. Rival networks, wallets, and fintech issuers will need to match Visa’s distribution, compliance reach, and merchant acceptance if they want to compete at scale.

The card boom has put stablecoins in shoppers’ pockets instead of leaving them parked on exchanges. If volumes keep rising, the next wave of crypto users may not arrive through a trading screen at all. They may arrive through a tap-to-pay transaction that spends digital dollars before they ever think of themselves as on-chain users.

The post Visa Is Quietly Eating Crypto Payments As Card Spending Explodes 500% appeared first on Crypto Adventure.