Emotional trading destroys portfolios. Here is the exact blueprint, code, and infrastructure required to build, host, and execute a systematic algorithmic trading bot on Binance.

⏱️ Estimated reading time: 18–22 minutes

I remember the exact moment I stopped trading manually. It was 3:14 AM. I woke up, instinctively reached for my phone, and opened the Binance app. The screen was painted red. A sudden 10% market drop had blown past my mental stop-loss, liquidating a significant position while I was unconscious.

Crypto is a brutal, unforgiving arena. It operates 24/7, 365 days a year. It doesn’t care about your sleep schedule, your stress levels, or your “gut feeling.”

If you are clicking buttons on an exchange interface, you are already the yield. You are competing against institutional algorithms, high-frequency market makers, and quants who execute trades in milliseconds. To survive, you must stop acting like a gambler and start building like an engineer. You need a machine.

Most retail traders fail not because their ideas are entirely wrong, but because their execution is fundamentally flawed.

Humans suffer from FOMO (Fear Of Missing Out) and panic. We hold losers too long hoping they bounce back, and cut winners too early out of fear. Furthermore, by the time your eyes process a chart pattern and your finger clicks “Buy,” an algorithm has already entered the trade, captured the spread, and is preparing to exit.

To build an edge, we must remove the human bottleneck. We need a system that calculates probabilities, manages risk with ruthless precision, and executes orders automatically.

Algorithmic trading is not magic; it is simply the automation of logic. We are looking for statistical inefficiencies in the market that occur frequently enough to generate a positive expected value over thousands of iterations.

One of the most robust inefficiencies in ranging cryptocurrency markets is Mean Reversion. The premise is simple: assets overreact to short-term news and liquidity crunches, causing their prices to stretch too far from their historical averages. Like a rubber band, when the price stretches too far, it snaps back.

Our goal is not to predict the macroeconomic future of Bitcoin. Our goal is to catch the rubber band snapping back.

To quantify the “stretch,” we will build a strategy combining two powerful mathematical concepts: Bollinger Bands (Volatility) and the Relative Strength Index (Momentum).

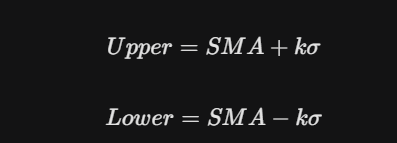

Bollinger Bands measure market volatility using a Simple Moving Average (SMA) and standard deviations. The bands expand during high volatility and contract during consolidation.

The middle band is an $n$-period moving average:

The upper and lower bands are calculated by adding and subtracting $k$ standard deviations ($\sigma$) from the SMA:

For our strategy, we will use a 20-period SMA ($n=20$) and a 2 standard deviation multiplier ($k=2$). When the price pierces the lower band, it is mathematically oversold relative to recent volatility.

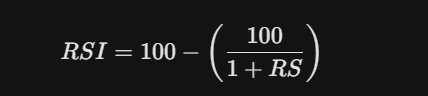

While Bollinger Bands tell us about price extremes, RSI measures the velocity of price movements. It oscillates between 0 and 100.

Where $RS$ is the average of $n$ days’ up closes divided by the average of $n$ days’ down closes.

The Trade Logic:

This creates a high-probability, short-term reversion trade.

To build this, we will use Python. It is the undisputed king of quantitative finance due to its data manipulation libraries.

You will need to install a few core libraries.

Run this in your terminal:

pip install ccxt pandas pandas_ta python-dotenv

Create a .env file in your project directory:

BINANCE_API_KEY=your_api_key_here

BINANCE_SECRET=your_secret_key_here

Here is the production-ready logic for our Mean Reversion bot.

import ccxt

import pandas as pd

import pandas_ta as ta

import time

import os

from dotenv import load_dotenv

# Load secure credentials

load_dotenv()

class MeanReversionBot:

def __init__(self, symbol, timeframe, trade_size):

self.symbol = symbol

self.timeframe = timeframe

self.trade_size = trade_size # Amount in USD

self.in_position = False

self.buy_price = 0

# Initialize Binance via CCXT

self.exchange = ccxt.binance({

'apiKey': os.getenv('BINANCE_API_KEY'),

'secret': os.getenv('BINANCE_SECRET'),

'enableRateLimit': True,

})

def fetch_data(self):

"""Fetches historical OHLCV data from Binance and returns a DataFrame."""

try:

bars = self.exchange.fetch_ohlcv(self.symbol, timeframe=self.timeframe, limit=100)

df = pd.DataFrame(bars, columns=['timestamp', 'open', 'high', 'low', 'close', 'volume'])

df['timestamp'] = pd.to_datetime(df['timestamp'], unit='ms')

return df

except Exception as e:

print(f"Error fetching data: {e}")

return None

def apply_indicators(self, df):

"""Calculates Bollinger Bands and RSI."""

# 20-period, 2 StdDev Bollinger Bands

df.ta.bbands(length=20, std=2, append=True)

# 14-period RSI

df.ta.rsi(length=14, append=True)

return df

def execute_trade(self, side, price):

"""Executes market orders securely."""

try:

ticker = self.exchange.fetch_ticker(self.symbol)

current_price = ticker['last']

# Calculate quantity based on USD trade size

amount = self.trade_size / current_price

# Use market orders for guaranteed execution (warning: subject to slippage)

order = self.exchange.create_market_order(self.symbol, side, amount)

print(f"SUCCESS: {side.upper()} order placed at {current_price}. Order ID: {order['id']}")

return True, current_price

except Exception as e:

print(f"Trade Execution FAILED: {e}")

return False, 0

def run(self):

print(f"Starting Quant Bot for {self.symbol} on {self.timeframe} timeframe...")

while True:

df = self.fetch_data()

if df is None:

time.sleep(10)

continue

df = self.apply_indicators(df)

last_row = df.iloc[-1]

# Extract indicator values safely

close = last_row['close']

lower_band = last_row['BBL_20_2.0']

middle_band = last_row['BBM_20_2.0']

rsi = last_row['RSI_14']

print(f"Price: {close} | L-Band: {lower_band:.2f} | RSI: {rsi:.2f} | Position: {self.in_position}")

# ENTRY LOGIC

if not self.in_position:

if close < lower_band and rsi < 30:

print("Entry Signal Triggered! Market is oversold.")

success, exec_price = self.execute_trade('buy', close)

if success:

self.in_position = True

self.buy_price = exec_price

# EXIT LOGIC

elif self.in_position:

# Target: Mean Reversion to the SMA

if close > middle_band:

print("Take Profit Triggered! Reverted to mean.")

success, _ = self.execute_trade('sell', close)

if success:

self.in_position = False

self.buy_price = 0

# Stop Loss: 3% drawdown

elif close < (self.buy_price * 0.97):

print("Stop Loss Triggered! Cutting losses.")

success, _ = self.execute_trade('sell', close)

if success:

self.in_position = False

self.buy_price = 0

# Wait for next candle (avoiding API rate limits)

time.sleep(60)

if __name__ == "__main__":

# Trade $100 worth of ETH/USDT on the 15-minute timeframe

bot = MeanReversionBot(symbol='ETH/USDT', timeframe='15m', trade_size=100)

bot.run()

Running this script on your local laptop is a recipe for disaster. If your Wi-Fi drops, your computer goes to sleep, or a Windows update forces a restart, your bot dies — potentially while holding an unhedged position.

You must deploy your bot on a VPS (Virtual Private Server) in the cloud.

Binance matches orders globally, but historically, their primary matching engines for AWS users have fast routing via AWS Tokyo (ap-northeast-1) or AWS Europe. For cost efficiency, DigitalOcean or AWS EC2 (Free Tier) are perfect.

sudo apt update

sudo apt install python3-pip tmux

tmux new -s tradingbot

python3 bot.py

Press Ctrl+B, then D to detach. Your bot is now running quietly in the cloud, 24/7.

If algorithmic trading were as easy as copying and pasting a script, everyone would be a billionaire. Here is the reality check that fake guru “bot builders” will never tell you.

1. Slippage and Trading Fees Binance charges a 0.1% fee on spot trades. To buy and sell, you pay 0.2% total. If your bot targets microscopic 0.15% profit margins, you will mathematically bleed to death through fees. Your strategy’s target profit must be significantly higher than the exchange fees plus expected slippage (the difference between the price you see and the price your market order actually fills at).

2. Regime Changes The bot we built is a Mean Reversion bot. It thrives in ranging, sideways markets. What happens when Bitcoin goes on a massive, structural bull run or a catastrophic bear market? The price will pierce the lower Bollinger Band, the bot will buy, and the price will just keep dropping, blowing past the stop-loss. Algorithms fail when market regimes change from “ranging” to “trending.” Real quants build regime filters (like using the ADX indicator) to turn the bot off during strong trends.

3. API Rate Limits Binance allows you to send a specific number of requests per minute (usually around 1200 weight). If you query the exchange every second, you will get IP banned. The code above uses ccxt's enableRateLimit: True and a time.sleep(60) to protect you from this.

Building trading systems taught me more about markets than years of staring at charts.

Algorithmic trading is the ultimate intersection of finance, mathematics, and software engineering. We started by defining a human problem — emotional, slow trading — and built an automated, cloud-hosted machine to solve it based on statistical probabilities.

You now have the framework, the math, and the Python execution engine. Start small. Test extensively. The market will always be there, but now, you don’t have to stay awake to trade it.

If this gave you a new perspective on systematic trading or saved you hours of debugging API docs, feel free to clap — it helps more builders and traders discover this playbook. Follow me for more deep dives into quantitative systems and engineering.

If you enjoyed this, please:

Thanks for reading!

Questions? Find me on:

Also, Telegram for free trading signals. No privet or pay groups.

Disclaimer: Cryptocurrency trading involves significant risk. This article is for informational purposes only and does not constitute financial advice.

Building a Binance Trading Bot That Actually Works was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.