Europe is not losing the stablecoin debate because it lacks regulation.

It is losing because regulation is not the same thing as adoption.

That is the uncomfortable truth behind the current stablecoin conversation in Europe: the region has built some of the strongest rules in the world, but the market is still moving toward dollar liquidity, dollar rails, and dollar-denominated digital money.

Christine Lagarde put it bluntly. The case for euro-denominated stablecoins, she said, is “far weaker than it appears.” Isabel Schnabel went further, warning that rising use of stablecoins could “cement the dollar’s global dominance.”

Those are not casual remarks. They are signals. And they tell us that the real debate is no longer about whether stablecoins matter. It is about who gets to shape the future payment stack and which currency becomes its default unit of account.

Europe is strong on policy seriousness. It is trying to preserve the euro’s role before digital dollarisation becomes entrenched.

On regulation, Europe is ahead.

MiCAR provides the EU with a formal framework for issuance, reserves, authorisation, disclosure, and supervision. That matters because it removes ambiguity and creates a legal perimeter for digital assets. For banks, payment firms, and institutions, this is not a minor detail. It is the difference between cautious experimentation and credible participation.

The European Central Bank is also pushing the digital euro as a strategic answer to Europe’s dependency on non-European payment infrastructure. Reuters reported that the European Parliament backed the digital euro in June 2026, and ECB officials have indicated that 2029 is a realistic launch horizon.

So yes, Europe is doing something serious. It is building the scaffolding for monetary sovereignty. It is not ignoring the future of money. It is trying to govern it before the market governs Europe instead.

But policy strength does not automatically translate into market power.

The ECB has warned that rising stablecoin use could reinforce dollar dominance, weaken some countries’ ability to set monetary policy, and reduce the euro’s influence. Schnabel’s warning is especially important because it frames stablecoins not as a niche crypto issue, but as a structural monetary one.

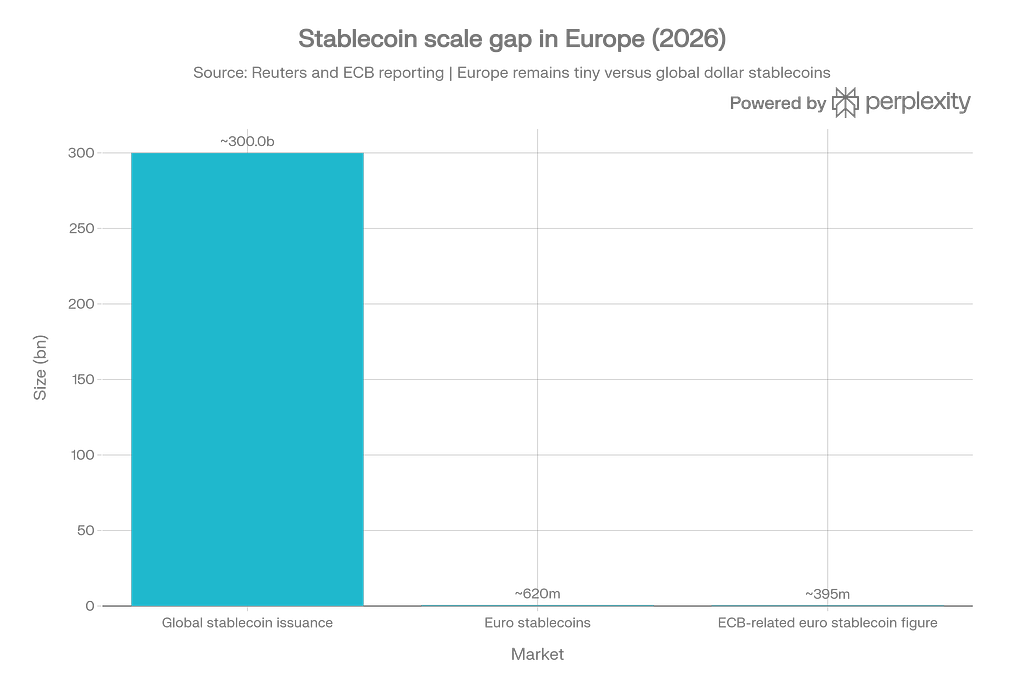

The numbers tell the same story.

Reuters has reported global stablecoin issuance at nearly USD 300 billion, while euro-denominated stablecoins totalled only about USD 620 million. In another ECB-related context, Reuters cited euro stablecoins at roughly EUR 395 million.

That is not an ecosystem on the brink of global dominance. It is a gap. And gaps matter, because network effects compound. The currency that becomes the default for cross-border settlement, treasury flows, and tokenised finance tends to remain so.

This is why the sovereignty argument is so important. Europe is not trying to “win” stablecoins in the same way a startup wins product-market fit. It is trying to prevent USD stablecoins from becoming the invisible default inside European commerce. That is a defensive strategy, not an offensive one.

Europe is not building the dominant stablecoin market. It is trying to avoid becoming a captive market for someone else’s currency rails.

Lagarde’s scepticism is not just ideological. It is rooted in how stablecoins behave under stress.

In her speech, she said stablecoins are vulnerable to runs and that their trade-offs outweigh the short-term benefits they might bring in financing conditions and global reach. She also argued that they are not the right tool for strengthening the euro’s international role.

That is a subtle but important point. The ECB is not saying tokenisation is bad. It is saying that settlement should not depend on a privately issued instrument that can lose its peg under pressure. In other words, the ECB distinguishes between the technology and the asset. It wants the technology, but it does not trust the cash leg.

Lagarde has instead pointed toward tokenised commercial bank deposits as a safer alternative. That tells us something important: Europe’s preferred path is not to expand stablecoins at any cost. It is to preserve the euro's monetary function while allowing digital innovation in forms the ECB considers more stable.

The UK is moving with a more enabling posture.

The Bank of England recently softened its stablecoin rules, dropped proposed individual holding caps, set a GBP 40 billion issuance limit per stablecoin, and raised the reserve allocation to short-term government debt.

That may still be cautious, but it is clearly more market-oriented than Europe’s position. The UK is essentially saying: let stablecoins prove their value under supervision, and then manage the risk. Europe is saying: contain the risk first, and only then decide how much room the market gets.

For founders and CEOs, that difference is not academic. It affects where innovation happens first, where capital feels more comfortable, and where product teams can move faster without running into a wall of regulatory resistance.

The UK is more willing to let the market test scale. Europe is more determined to protect the perimeter.

Europe does not have a vision problem. It has a conversion problem.

There is no shortage of policy awareness or concern about dollar dominance. What is missing is a euro-native product layer with enough liquidity, adoption, and utility to compete with the existing USD ecosystem. Bank-led euro stablecoin projects are a step in that direction, but they are still catch-up moves.

This is where the strategic reality becomes uncomfortable. Europe may have the strongest regulatory architecture, but that strength does not matter if users, treasuries, merchants, and developers continue to default elsewhere. Regulation can defend a market. It cannot create one.

That is the tension at the heart of monetary sovereignty. It is not about whether Europe has rules. It does. It is about whether those rules will be enough to keep the euro relevant in a world where digital money is becoming programmable, composable, and borderless.

If you are building in fintech, payments, or crypto, this debate is not theoretical.

The next phase of digital money will not be decided by ideology. It will be decided by who can combine compliance, liquidity, and utility at scale.

That means the winners will be the firms that understand reserve design, redemption trust, distribution, and the regulatory logic of each market. In Europe, the challenge is not just to launch a product. It is to launch a product that can survive scrutiny, earn trust, and still attract users at scale.

And that is why this topic matters beyond policy circles. It is a question of competitiveness. It is a question of architecture. It is a question of whether Europe wants to be a builder of digital money or simply the best-regulated place to consume it.

Europe is not failing because it lacks vision. It is failing because regulation is not enough to create market momentum.

The ECB is right to worry about dollar stablecoins becoming embedded in European commerce. But concern alone will not produce a dominant euro stablecoin. That requires product, liquidity, distribution, and user behaviour. On those dimensions, Europe is still behind.

So the real stablecoin debate in Europe is not whether to regulate the future.

It is a question of whether Europe still knows how to build one.reuters+2

Europe is winning on rules, but losing on market momentum.

Joseph Zammit is a CMO and CSO in fintech and crypto with 25+ years at the intersection of marketing, strategy, and regulation. He helped design Malta’s pioneering DLT framework, launched the country’s first neobank, and led global expansion for crypto and Web3 platforms, turning complex regulatory and market conditions into clear go‑to‑market decisions. He is a member of the Crypto Valley Association.

The Real Stablecoin Debate in Europe Is About Monetary Sovereignty was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.