Few companies have shaped the modern digital economy as profoundly as Microsoft. Once known primarily for the Windows operating system and Office software, the company has successfully reinvented itself as a global leader in cloud computing and artificial intelligence. Under the leadership of Satya Nadella, Microsoft has transformed into a platform-driven technology powerhouse, with Azure cloud services, AI integration, and enterprise software subscriptions fueling a new era of growth.

But with the stock already among the most valuable in the world, investors are asking a crucial question: Does Microsoft still offer attractive upside, or has the AI-driven optimism already been priced in? A deeper look at the company’s financial performance, competitive advantages, and valuation may provide the answer.

Microsoft is a global technology leader operating across software, cloud infrastructure, enterprise services, and consumer hardware. Its core businesses include Windows, Microsoft 365, Dynamics 365, LinkedIn, GitHub, and the Azure cloud platform. Azure remains the strategic centerpiece, powering enterprise AI workloads and hybrid cloud deployments. The company continues to expand its AI capabilities through acquisitions, internal R&D, and deep integration across its software ecosystem.

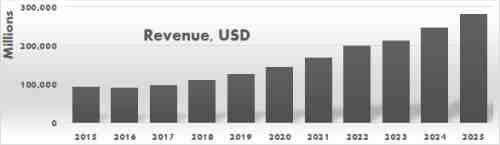

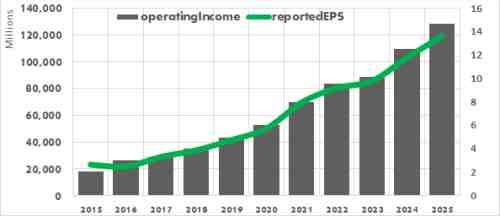

Microsoft’s financial performance remains robust, supported by strong cloud and software demand.

Analysts project:

Bank of America forecasts 15–17% annual revenue growth over the next three years, with Intelligent Cloud expanding 24–28%. Operating margins are expected to remain above 46% despite rising AI‑related capex.

MSFT currently trades around $366, down from its 52‑week high of $555.45. The stock has faced short‑term pressure due to concerns around Copilot execution and rising capex, but long‑term sentiment remains strongly bullish.

Wall Street’s average 12‑month price target is $586–603, implying ~55% upside.

The stock price has risen by more than 413 229% since the IPO.

Microsoft pays a $0.91 quarterly dividend ( 0.99% yield) and just hiked it again — payout ratio still only ~22%. In the latest quarter alone it returned $12.7 billion via dividends plus repurchases, backed by a multi-billion-dollar authorization. It’s the perfect mix: income today plus steady share-count reduction that juices EPS growth tomorrow.

Microsoft outpaces rivals in cloud profitability and AI readiness. Here’s how the big four stack up right now:

MSFT offers the best blend of growth, margin, and yield — exactly what both institutional portfolios and retail accounts crave.

Microsoft just froze hiring in cloud and sales groups, a classic efficiency move while pouring billions into AI infrastructure. At the same time, Copilot leadership changes and fresh AI talent hires signal aggressive execution on the next growth wave. Short-term it may trim costs; longer-term it reinforces Microsoft’s AI moat and supports a premium valuation — good news for anyone holding or buying the dip.

You must log in to view this content.

Curious whether your favorite company is undervalued or overpriced?

We provide independent stock valuation reports based on:

📩 Order a custom stock valuation report and discover the true value behind the ticker.

Perfect for:

👉 Send your ticker and receive a detailed valuation report.

More US Stocks price targets!

Originally published at https://aipt.lt on March 27, 2026.

Microsoft: High Growth, High Margins, High Expectations was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.