From the lens of 7 years in the trenches of crypto, one first principle has proven itself time and again: capital is like water; it will always find the path of least resistance to the highest ground. Regulation can build dams and divert streams, but it rarely stops the river from flowing. We are seeing a masterclass in this dynamic play out right now in the stablecoin market.

Since the landmark U.S. GENIUS stablecoin bill [link to official bill text or a high-authority news source] was signed on July 18, a specific segment of the market has erupted. Far from being a headwind, the legislation has acted as a powerful, albeit unintentional, catalyst. By prohibiting stablecoin issuers from directly paying yield to holders, the law has inadvertently funneled billions of dollars into protocols that offer yield through other mechanisms.

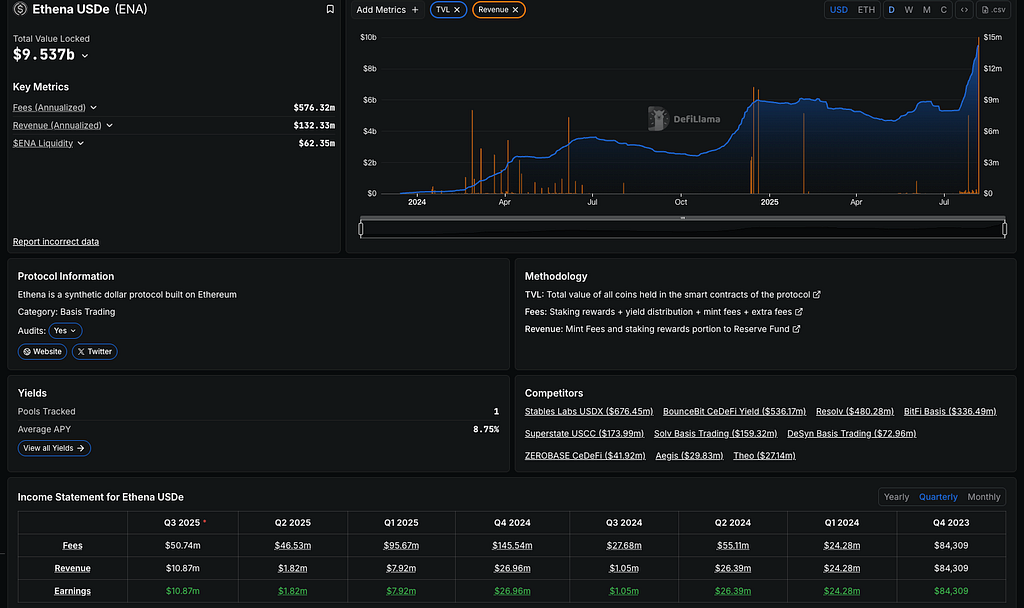

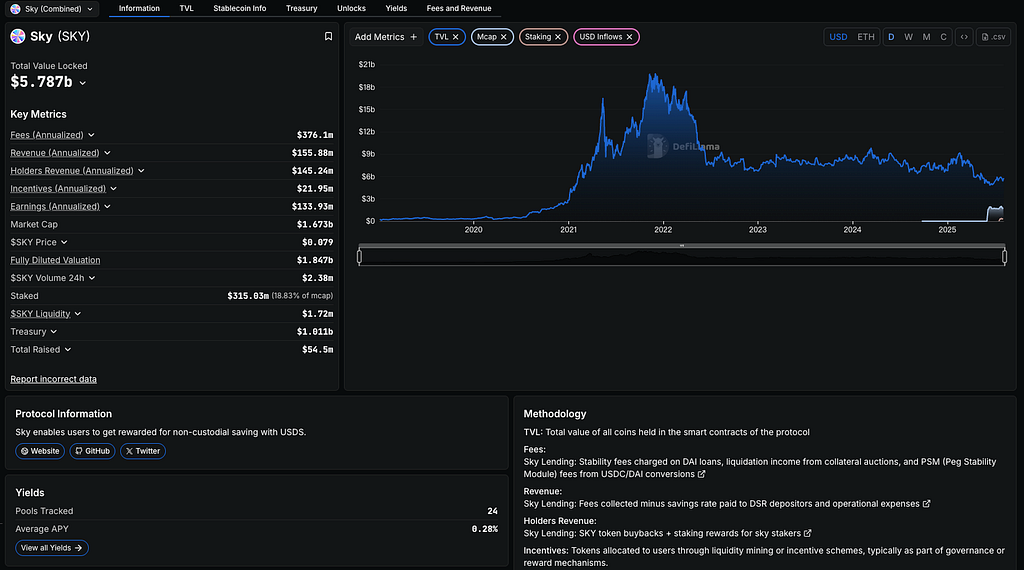

The two clearest beneficiaries of this capital rotation are Ethena’s USDe and Sky’s USDS. The data tells a compelling story.

To understand this shift, it’s crucial to distinguish between the two models:

The market’s reaction was swift and decisive. Investors, now unable to receive yield directly from an issuer, have turned to protocols where they can stake their stablecoins to capture protocol-generated revenue.

1. Ethena (USDe): The High-Octane Beneficiary

Ethena has been the breakout winner. As shown on DeFiLlama [link to the Ethena page on defillama.com], its synthetic dollar, USDe, has seen its circulating supply explode by a staggering 70% since the bill’s signing, rocketing to nearly $9.5 billion. This has propelled USDe to become the third-largest stablecoin by market capitalization, a stunning ascent for a protocol that generates yield via a sophisticated basis trading strategy.

The allure is obvious: a market-leading 10.86% APY for those who stake their USDe for sUSDe. For capital seeking yield, Ethena became the most attractive port in the post-GENIUS storm.

2. Sky (USDS): The Steady Incumbent

Sky’s USDS, another major player in the yield-bearing space, has also reaped significant benefits. Its supply has grown by a healthy 23% in the same period, reaching approximately $4.8 billion and securing its position as the fourth-largest stablecoin.

While its staking APY of 4.75% is more conservative than Ethena’s, it represents a stable and attractive return for a different risk profile. The protocol, which allows users to earn rewards for non-custodial saving, has proven to be a reliable alternative for those seeking sustainable yield.

What we are witnessing is not a loophole; it’s a feature of open, permissionless systems interacting with closed, permissioned regulatory frameworks.

This regulatory catalyst has fundamentally reshaped the competitive landscape. The question is no longer just about peg stability and liquidity, but about capital efficiency and yield-generation architecture.

The surge in USDe and USDS poses a direct challenge to the incumbent non-yield-bearing giants. While a flight to safety will always preserve a role for assets like USDT and USDC, the gravitational pull of sustainable, mid-to-high single-digit APY is undeniable, especially in a world of persistent inflation.

As builders and investors, we must now ask: Will regulators attempt to address this “indirect” yield, or will they accept it as a market-based solution? How will this new paradigm influence the design of future stablecoins?

The GENIUS Act intended to bring order to the stablecoin market. In a classic crypto paradox, it has done so, but in a way that has unleashed a Cambrian explosion of innovation and capital flow in a direction few policymakers likely foresaw. The river has found its new course.

The GENIUS Act Paradox: How Banning Direct Yield Ignited a Stablecoin Surge was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.