What should have been simple took four business days, cost me over $45 in fees, and left both of us frustrated with unclear tracking. The recipient finally got the funds after navigating their local bank’s restrictions. That experience is far too common and it’s exactly why stablecoins are quietly transforming how we move money.

In 2026, stablecoins like USDC and USDT (the digital dollar) are no longer just crypto experiments. They’re becoming the smarter, faster choice for real-world payments. For fintech enthusiasts, crypto users, businesses, and everyday people sending money across borders, stablecoins and crypto payments offer clear advantages over traditional bank transfers, especially in cross-border payments.

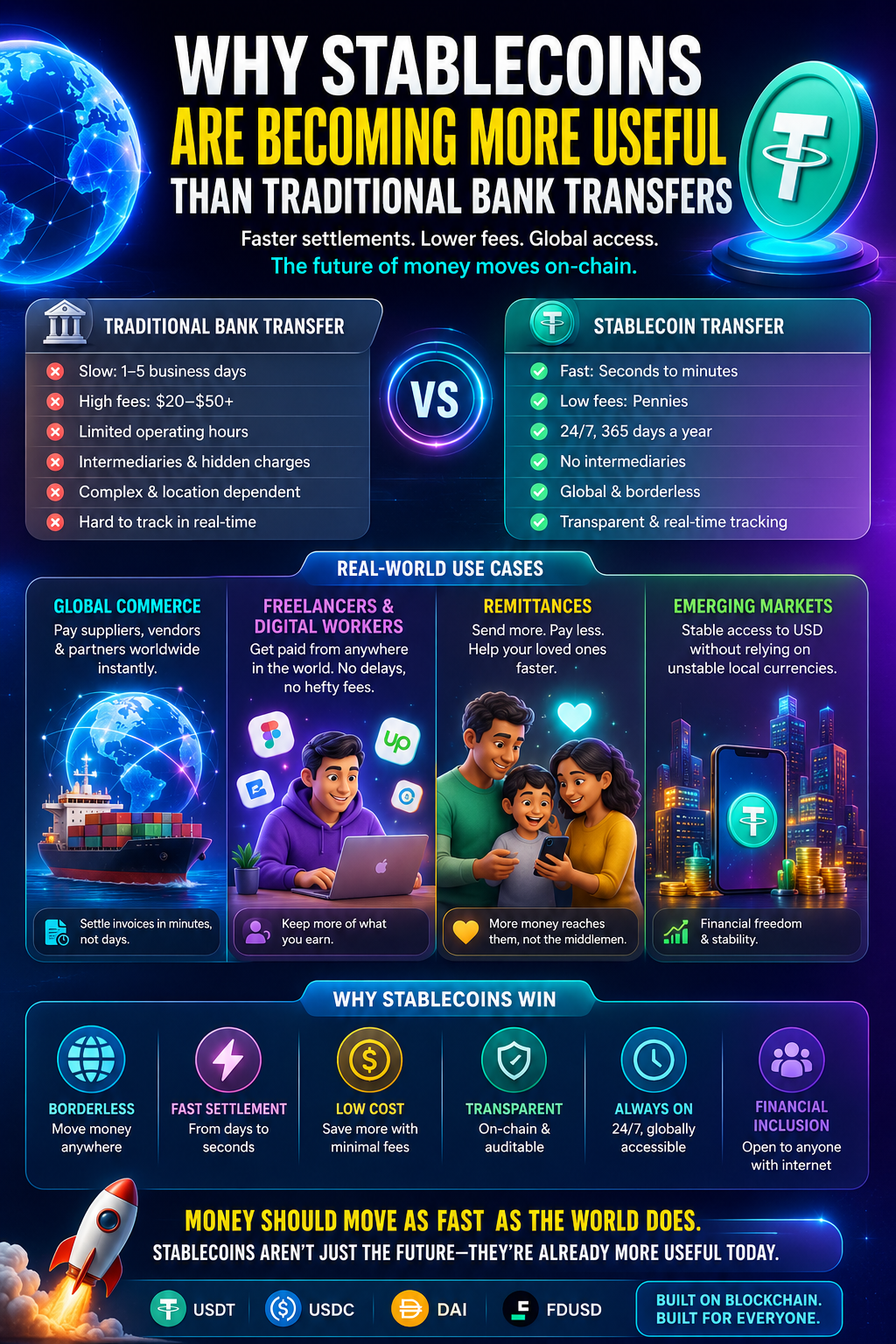

Traditional bank transfers, especially international ones, rely on legacy systems like SWIFT. These often take 1–5 business days to settle. Weekends, holidays, and banking hours create delays. Multiple correspondent banks add layers of fees typically 3–6.5% for remittances plus hidden FX spreads.

Cash flow suffers. A small business waiting for an overseas payment might delay payroll. A family relying on remittances sits in uncertainty. Transparency is limited you get a reference number and hope for the best.

This friction hurts global commerce, freelancers, and families sending money home.

Stablecoins are digital assets pegged to stable currencies, most commonly the US dollar. USDC, backed by cash and Treasuries with regular attestations, and USDT offer the reliability of fiat with the speed and borderless nature of blockchain.

They function as a digital dollar you can send anywhere with an internet connection. No need for a traditional bank account on the receiving end in many cases just a crypto wallet. Transactions settle in seconds to minutes, 24/7, with full visibility on the public ledger.

Speed is where stablecoins shine brightest.

While a cross-border wire might take days, stablecoin transfers confirm in seconds or minutes. This operates around the clock, ignoring time zones or holidays. For exporters, marketplaces, or anyone managing cash flow, this is game-changing. Funds arrive when needed, not when banks decide.

In fintech operations, this near-instant settlement reduces counterparty risk and eliminates the need for large pre-funded accounts abroad.

Businesses engaged in international trade are adopting crypto payments rapidly. Suppliers in Asia can receive payment from European buyers the moment a shipment is confirmed, thanks to smart contracts.

Stablecoins cut out multiple intermediaries, lowering costs dramatically often to under 1% all-in. This efficiency opens new markets, especially in regions with underdeveloped banking infrastructure. Companies maintain better liquidity and respond faster to opportunities in the global economy.

The gig economy has exploded, with millions of freelancers working for clients across continents. Traditional payouts via PayPal or wires still carry delays and fees that eat into earnings.

With stablecoins, platforms can pay creators and freelancers instantly upon milestone completion. A designer in Nigeria working for a US startup gets paid in digital dollar the same day no waiting, minimal fees, and the ability to hold or convert value as needed. Many freelancers now receive 30–35% of income this way, boosting their international competitiveness.

This instant crypto payments model gives workers greater financial control and predictability.

Remittances represent a massive $900+ billion market annually, critical for many developing economies. Traditional channels charge an average of 6.49% for sending $200.

Stablecoins slash these costs significantly often to under 1%. Families receive more of the money sent home, which studies link to meaningful poverty reduction. In places like Latin America, Africa, and parts of Asia, stablecoins also serve as a hedge against local currency volatility, giving recipients a stable digital dollar they can use or convert locally.

Adoption is growing fast: stablecoins already handle a substantial portion of flows in key corridors, with users citing speed and lower fees as top reasons.

Beyond speed, the economics favor stablecoins. Network fees are often pennies, with transparent, predictable costs. Every transaction is recorded on-chain, creating an immutable audit trail invaluable for businesses and compliance teams.

In contrast, traditional cross-border payments involve opaque intermediary charges and FX markups that add up quickly.

Stablecoins aren’t perfect. Regulatory clarity is improving but varies by country. Volatility in on/off-ramps and crypto wallet usability can still challenge less tech-savvy users. Security requires good practices lost keys mean lost funds, unlike bank protections.

Adoption also depends on integration with local systems for easy fiat conversion. However, major players like Visa, Stripe, and banks are building bridges, making stablecoins more accessible.

By 2026, stablecoin market capitalization has surpassed $300 billion, with trillions in annual transaction volume much of it real economic activity in payments and remittances.

As regulations mature and infrastructure improves, stablecoins will integrate deeper into everyday fintech tools. We’ll see more seamless experiences where users don’t even realize they’re using blockchain rails.

For global commerce, freelancers, and families, this means money that moves as fast as information finally closing the gap between our digital world and outdated financial plumbing.

I’ve talked to founders, freelancers, and families who’ve switched to stablecoins for cross-border payments. The common theme? Relief. Relief from waiting, high fees, and uncertainty.

Stablecoins don’t replace all traditional banking, but for speed, cost, and global reach, they’re often more useful today. As the digital dollar gains trust and utility, more people will wonder why they ever waited days for a transfer that can happen in minutes.

The future of money isn’t just digital it’s instant, open, and empowering. Whether you’re running a fintech startup, freelancing globally, or supporting family abroad, stablecoins and crypto payments are tools worth understanding now.

Are you already using them? The shift is happening faster than many expected and it’s making the world a little smaller and fairer, one borderless transaction at a time.

Why Stablecoins Are Becoming More Useful Than Traditional Bank Transfers was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.