In a policy statement published on June 22, 2026, the Bank of England set out revised draft rules for sterling-denominated systemic stablecoins, the large stablecoins used in mainstream payments rather than for crypto trading. The headline change is the removal of the holding limits proposed in the November 2025 consultation, which would have capped individuals at £20,000 and businesses at £10 million in any systemic stablecoin.

In their place, the Bank introduced a temporary issuance guardrail set initially at £40 billion (roughly $52.8 billion) per systemic stablecoin. Deputy Governor for Financial Stability Sarah Breeden described the package as “a major milestone in delivering greater choice and innovation in UK payments.” The Bank says the guardrail will be reviewed regularly and removed once risks to credit provision have been addressed.

The distinction between the old and new approach is the core of the story. The original holding caps were a demand-side restriction: they limited what any individual or business could hold, which industry stakeholders argued would make UK stablecoins impractical for institutional and corporate use. The new issuance guardrail is a supply-side tool: it limits how large a single stablecoin can grow in total, while letting individuals and businesses use it without any limit on the size, frequency, or type of transaction.

The Bank’s own framing is that the two approaches achieve a similar level of risk mitigation, the guardrail was calibrated using the same analysis that underpinned the holding limits, while being, in its words, cheaper and easier to implement. So this is best understood not as the Bank abandoning oversight, but as relocating it: from monitoring millions of individual wallets to capping issuance at the product level, which is far simpler to enforce and far less restrictive for end users.

| Element | November 2025 Proposal | June 2026 Revision |

|---|---|---|

| Individual holding cap | £20,000 per person | Removed, no holding limit |

| Business holding cap | £10 million per business | Removed, no holding limit |

| Growth control | Demand-side (per holder) | Supply-side: £40B issuance cap per stablecoin |

| User transactions | Constrained by holding cap | Unrestricted in size, frequency, type |

The other major industry complaint concerned reserves. The November 2025 proposal required systemic stablecoin issuers to hold at least 40% of their backing assets as unremunerated, meaning interest-free, deposits at the Bank of England, with up to 60% in short-term UK government debt (gilts). Industry analysis argued this was the heart of the viability problem: because the central bank deposits earned nothing, the structure carried a real cost. According to analysis by Range CEO Andres Monty reported by Decrypt, at gilt yields around 4%, the 40% interest-free floor could cost an issuer roughly £11.2 million a year for every £1 billion in circulation, a significant disadvantage versus US issuers under the GENIUS Act.

The logic is straightforward: gilts generate yield, while interest-free central bank deposits are a dead cost, so the more backing an issuer can hold in gilts rather than unremunerated deposits, the more viable the economics. Breeden had earlier acknowledged the original framework may have been “overly conservative” on this point. The exact revised split in the new draft should be confirmed against the final Code of Practice, but the direction of the Bank’s rethink, reducing the drag from unremunerated reserves, is aimed squarely at the complaint that UK issuance was uncompetitive.

The framework also clarifies a two-tier structure. The Financial Conduct Authority supervises non-systemic stablecoins, which covers the bulk of stablecoin activity today, including coins used for buying and selling crypto. Only once HM Treasury recognises a stablecoin as systemic, meaning large enough that problems could threaten financial stability, does the Bank of England’s regime apply, co-regulating alongside the FCA. The detailed transition framework between the two bodies, how responsibilities hand over as a stablecoin crosses into systemic territory, is one of the pieces still being finalised.

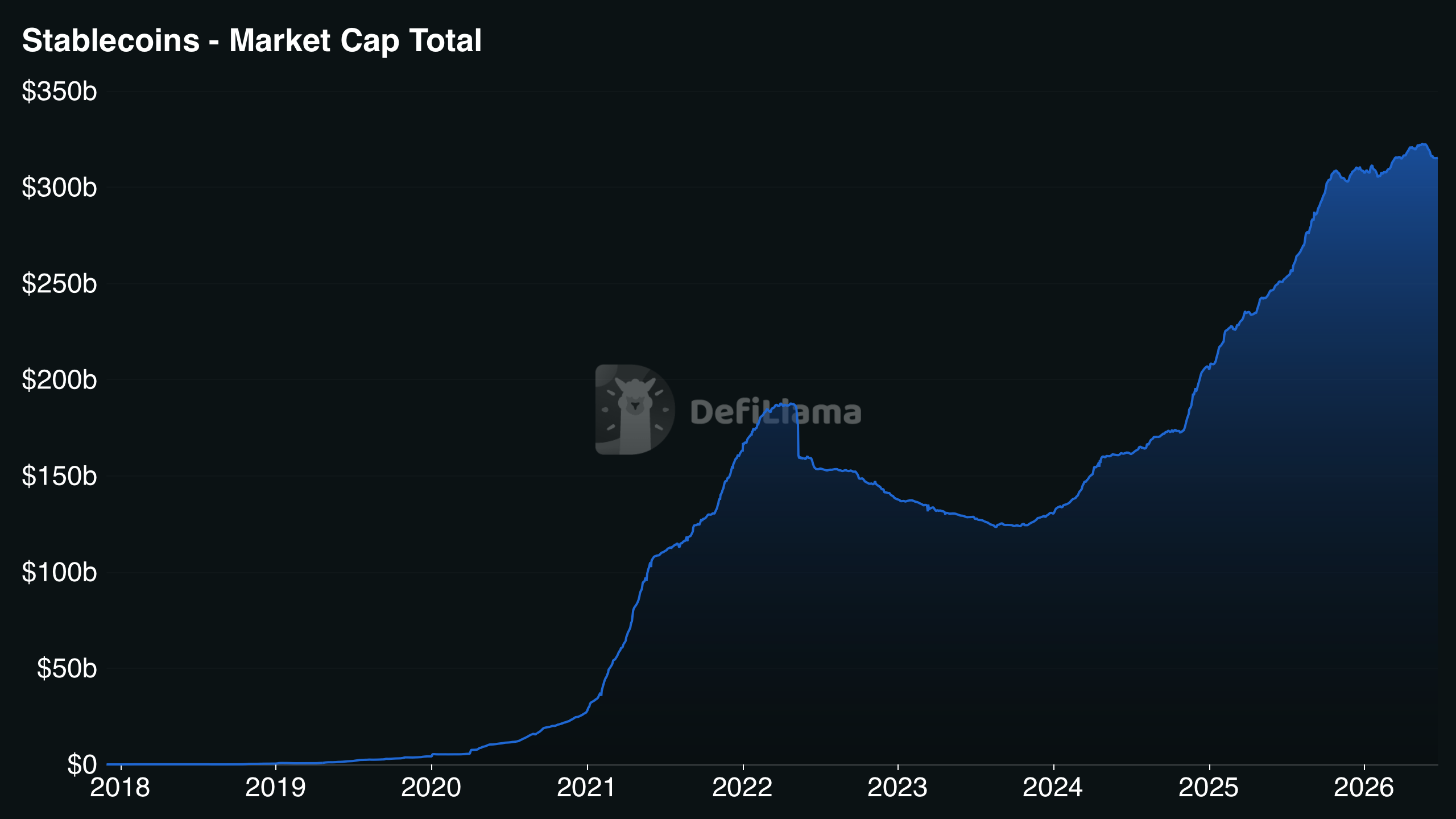

Non-dollar stablecoins collectively hold less than 0.5% of a roughly $315.278 billion global market at the time of writing, according to Defillama, with sterling-denominated tokens representing only a marginal slice of that already thin share.

The original framework drew warnings that GBP stablecoins might simply be issued from friendlier jurisdictions like Dublin rather than the UK. By shifting from user caps to an issuer cap and signalling relief on reserve costs, the Bank appears to be trying to keep stablecoin issuance onshore while preserving its financial-stability guardrails. Whether that balance holds is for the market and the consultation to test.

On the timeline, feedback on the draft closes on September 22, 2026. The Bank intends to finalise the Code of Practice by the end of 2026, which would allow regulated systemic stablecoins to operate in the UK from 2027. For now, the rules are a draft open to consultation, not a finished regime, but the direction, from restricting users toward capping issuers, marks a clear reorientation of how the UK intends to regulate this corner of the market.

The post Bank of England Ends User Limits in New Stablecoin Policy Shift appeared first on Coindoo.