Data published this week describe the same market from three altitudes: corporate treasury flows, derivatives positioning, and Fidelity’s long-run power law framework. Read together, they show a bottom being contested by completely different hands than the ones that built the top, and one veteran macro voice argues the process has just produced its first technical confirmation.

CryptoQuant analyst Darkfost wrote on X that the cumulative market capitalization of Bitcoin treasury companies has fallen from $396 billion in October 2025 to $272 billion, a loss of more than $100 billion, even as their combined holdings grew from 953,000 BTC to 1.14 million.

📉 The market cap of treasury companies has lost more than $100B since October 2025. Their holdings went from a valuation of $396B to $272B.

Over the same period, the number of BTC held by these companies increased from 953,000 BTC to 1.14 million now.

—> Since May, as BTC… pic.twitter.com/B9yvSaGON7

— Darkfost (@Darkfost_Coc) July 11, 2026

The timing of that growth is the uncomfortable part. The cohort tripled its Bitcoin position between November 2024 and October 2025, buying in a price range of $75,000 to $125,000, and since May, with the market trading far below that range, accumulation has slowed to nearly a halt. Strategy, the sector’s template, has started selling, per the same analysis.

The behavior inverts the thesis these companies sold to their shareholders. Treasury vehicles were pitched as price-insensitive permanent bids, buyers of every dip. The data instead shows procyclical buyers who scaled purchases with access to capital markets, and that access moves with their share prices. Falling equity valuations closed the financing channel that funded the buying, which means the corporate bid was never insensitive to price; it was leveraged to it. The cohort still holds more than 5% of Bitcoin’s supply, but as a source of new demand at these levels, it has effectively left the market.

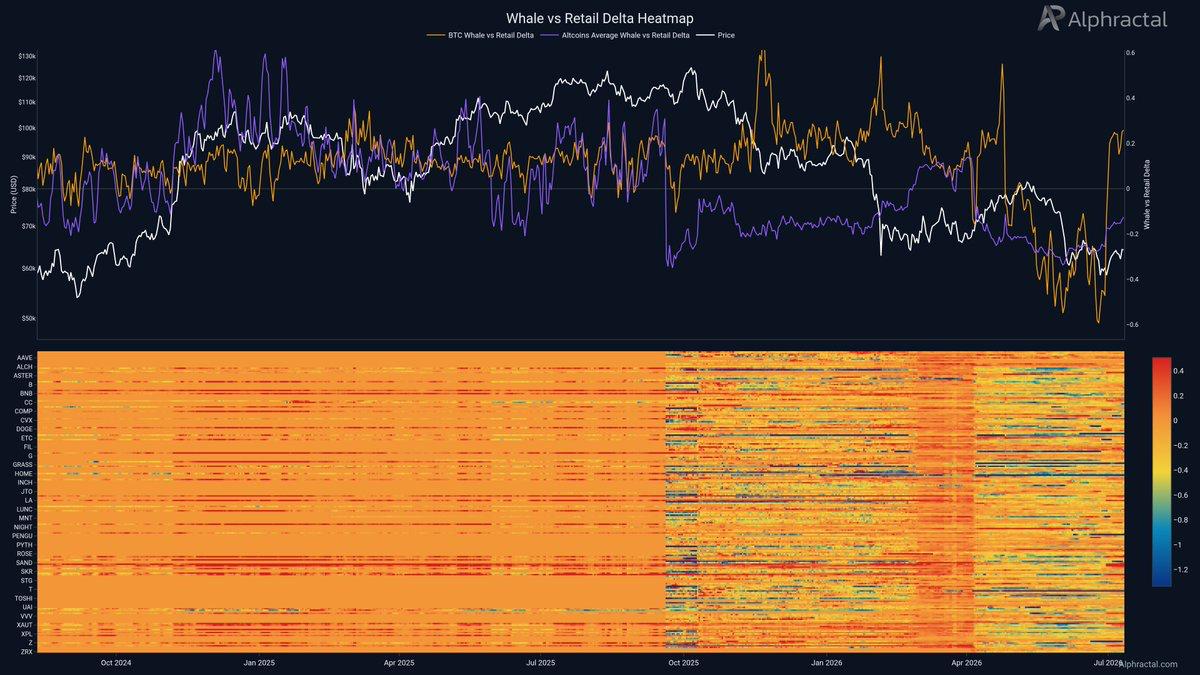

The bid that appeared where the corporate one vanished shows up in positioning data. Analytics firm Alphractal wrote also on X that its Whale vs. Retail Delta is rising again, meaning large positions have cut short exposure and added longs across the top 250 cryptocurrencies, with Bitcoin’s reading “even stronger than most altcoins.” Around the recent $58,000 bottom, the firm identified a sharp increase in whale long exposure, while smaller positions, the retail cohort, moved the opposite way and are positioned for further downside.

The split matters because of what each group’s track record at extremes looks like. Concentrated long positioning by large accounts at a local low, opposed by retail shorts, is the configuration that has historically marked accumulation phases rather than distribution ones. It is not a guarantee; Alphractal itself frames the open question as whether the whale flows represent conviction or a short-term trade around an oversold level. The honest version of the signal is directional but unproven: the biggest accounts on derivatives venues are treating $58,000 as a level worth owning, and the crowd is paying them funding to disagree.

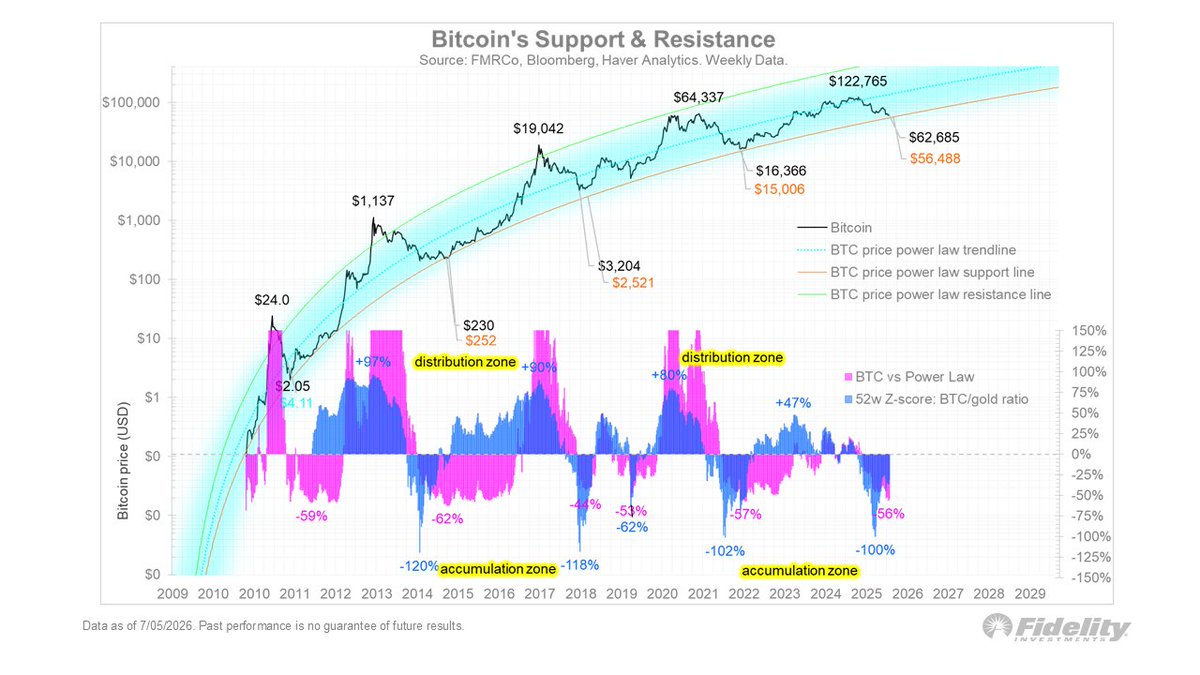

The third dataset supplies the frame the first two lack: where these prices sit in Bitcoin’s full history. Fidelity’s Bitcoin Support and Resistance chart, with data as of July 5, shows BTC trading in what the firm labels an accumulation zone and, in its words, “getting ever closer to its power law support line,” the lower boundary of the channel that has contained every cycle since 2010.

The chart marks recent price near $62,685 against a power law support line near $56,488, with the 52-week Z-score against gold pressing toward the negative extremes that previously appeared at the 2015, 2018-19, and 2022-23 cycle floors.

Power law models deserve their standard caveat: they are curve fits to a young asset’s history, not physical laws, and a first-ever break of the support line could simply mean the model was wrong. What the framework contributes here is not a price target but a classification. Every prior visit to this zone occurred when the marginal buyer had capitulated and ownership was migrating to longer-horizon holders, which is a reasonable description of corporates freezing while whales accumulate.

Jordi Visser, a macro strategist with more than three decades in institutional finance, put a trader’s structure on the same picture in an interview with Anthony Pompliano, published on July 11, 2026. “I finally got my first RSI divergence since the peak at the end of last year,” Visser said, pointing to Bitcoin printing a new low below $60,000 while the four-hour RSI held above its prior low. His plan is mechanical rather than prophetic: “Now I can buy something when we get back above 60, and I’ll just stop myself back out below the lows.”

His explanation for the weakness adds the macro layer the positioning data cannot see. Visser argued Bitcoin’s decline was partly a casualty of the AI infrastructure trade, with capital rotating out and Bitcoin serving as a high-beta funding and hedging instrument for investors holding semiconductor exposure. As that trade’s momentum faded and leverage came off, the selling pressure on Bitcoin began to ease, which in his framework is how bottoms start: “Price leads narrative. The first thing that always happens in a bottom is you start getting short covering.”

Visser also read the market’s response to Strategy’s sale, the event at the center of the treasury cohort’s freeze, as evidence of absorption rather than fragility. Bitcoin traded above the level where the sale occurred instead of breaking down on it. “Once you don’t sell off after something like that, it actually is more of a positive than a negative,” he said. His confirmation line sits well overhead at the 200-day moving average around $76,000-77,000: until price reclaims it, he treats the advance as a short-covering rally, not a reversed trend. He allows the range could still stretch to $50,000 or $45,000, while expecting Bitcoin above $100,000 within a year, and flagged the Federal Reserve’s July 29 meeting as a near-term catalyst, arguing that no hike could put Bitcoin above $70,000 as markets price out further tightening.

The synthesis across all four reads is a market changing hands rather than finding new ones. The measurable tells from here are specific to each actor. For the treasuries, the number to watch is whether cohort holdings resume growing at all below $65,000, or whether Strategy’s selling spreads to weaker balance sheets forced to liquidate into the low, which could be the bear case the retail shorts are betting on. For the whales, the Alphractal delta staying positive through the next leg, up or down, may separate conviction from a scalp.

The Fidelity support line near $56,500 converts from chart decoration into live test if the $58,000 low breaks. And Visser’s framework adds the two dates and one line that arbitrate everything above: the Fed’s July 29 decision, reclaiming $60,000 as the entry trigger, and the 200-day near $76,000 as the level that could turn a short-covering bounce into a confirmed reversal. A bottom built by whales against corporate paralysis is a narrower foundation than the one that built the top, but it is the foundation the market currently has.

The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency markets are volatile and involve substantial risk. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.

The post Bitcoin’s Bottom Hunt: What 4 Market Signals Show appeared first on Coindoo.