🚨 Nasdaq 100 dropped by 1.4% yesterday — its second-steepest fall since April’s tariff shock, led by Nvidia. While over 350 S&P 500 stocks rose, megacaps dragged the index down.

📉 Wall Street futures are also under pressure today:

🔹 US100, US500, US30 are down 0.3%–0.4%

🇪🇺 In Europe, DE40 and UK100 futures are slightly lower too.

⏳ Markets await:

🕘 Final Eurozone inflation data (09:00 GMT)

🕕 US FOMC minutes (18:00 GMT)

🗣️ Fed speakers Waller & Bostic

🇨🇳 PBoC kept its key rate unchanged at 3.5%, as expected.

📈 HK.cash and CHN.cash futures are up 0.5%

💱 Forex Focus:

🔻 EUR/USD slips 0.1%

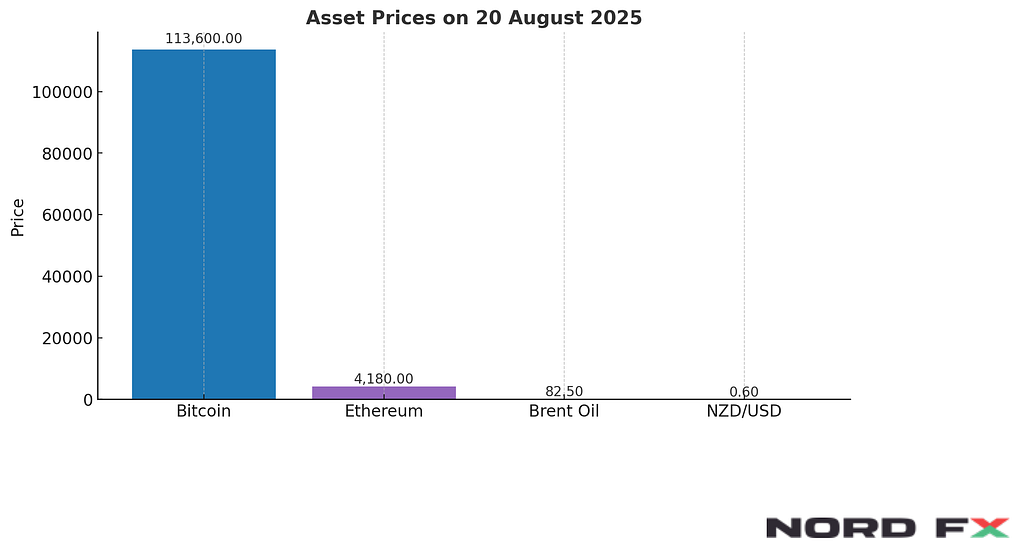

💥 NZD/USD is the most volatile pair today, down 1% after RBNZ cut rates to a 3-year low — more easing may follow. The ‘Kiwi’ is under pressure.

📉 US Treasury yields fall as markets await Powell’s Jackson Hole speech on Friday — 10Y yield drops to 4.31%.

💬 S&P Global Ratings: Tariff revenues may help offset tax cuts and support credit outlook.

🛢️ Commodities:

🟢 Oil rebounds 0.5% after a weak session and bullish US API data (-2.4M barrels).

⛽ Gasoline stocks also fell; NATGAS down 0.5%

💰 Crypto Corner:

🟠 Bitcoin is trying to stabilise around $113,600 after yesterday’s drop

🟣 Ethereum remains weak at $4,180 vs $4,700+ earlier this week

🔔 Volatility in metals remains low this morning.

📍 Stay informed, stay ahead — trade smarter with NordFX! 🚀

📊 Morning Market Update — 20.08.2025 was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.