Picture this: You’re sipping coffee, scrolling through your portfolio, and wondering where to park your next $10,000 for steady growth and juicy dividends. AbbVie catches your eye-a biotech titan with a 3% dividend yield and a stock up 23% in 2025, outpacing the market. Why care? Because AbbVie’s blend of innovation, cash flow, and resilience could be the anchor your investments need in today’s volatile world.

AbbVie operates as a global biopharma leader, focusing on immunology, oncology, neuroscience, and aesthetics through its Allergan arm. Key stars like Skyrizi and Rinvoq are surging, with combined 2025 sales projected over $25 billion, offsetting Humira’s biosimilar erosion. With 50,000 employees and a robust R&D pipeline-including obesity and migraine therapies-AbbVie is positioned for high single-digit revenue growth through 2029.

AbbVie’s Q2 2025 revenues hit $15.4 billion, up 6.6% year-over-year, driven by neuroscience’s 24% jump. Adjusted EPS rose 12% to $2.97, prompting an upward revision to $11.88-$12.08 for the year-excluding IPR&D hits. Trailing 12-month revenue stands at $58.3 billion, with a healthy 42% operating margin, though aesthetics dipped 8% on consumer softness.

Key ratios paint a stable picture: Debt-to-Equity at 17.9% (below S&P’s 20.9%), Cash-to-Assets at 4.7%, and ROE exceeding 140% -signaling efficient capital use for growth.

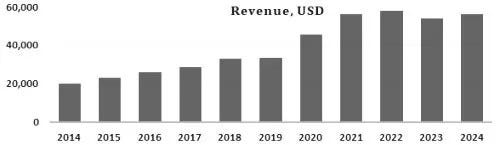

Over a 10-year period, the average annual revenue growth rate was nearly 11%. However, revenue growth in the most recent year was only 3.71%.

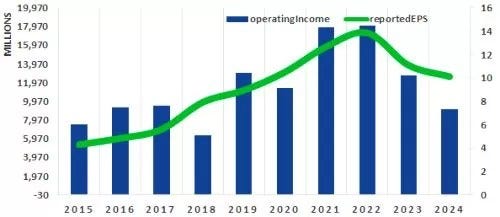

There is also a noted slowdown in EPS growth. Over a 10-year period, the average annual EPS growth was nearly 12%, but over the past 5 years, it was only 2.51%.

ABBV shares (NYSE: ABBV) have rocketed nearly 23% year-to-date through September 2025, outpacing the S&P 500’s 18% gain, fueled by immunology wins. Trading around $220, the stock hit a record high post-Rinvoq patent news, with a forward P/E of 15.9-premium yet justified by 8.4% projected CAGR through 2030. Volatility? Minimal-ABBV dipped just 23% in the 2022 bear market versus the index’s 25%.

The stock price has risen by more than 534% since the IPO.

Competitor Comparison Table

2025–2029 Price Targets:

*Theoretical calculation. Actual results may differ significantly due to market conditions as well as your investment strategy and tactics.

With the stock price near its all-time high (ATH), buying now may not be the best move. A correction is likely at some point, offering a chance to buy at a lower price. However, when investors see such price momentum, the fear of missing out (FOMO) often kicks in. It’s up to you to decide when to jump in-we’re waiting for a deeper correction before adding to existing positions.

On X, analysts are buzzing with upgrades.

AbbVie’s stock is flirting with all-time highs, but its Dividend King status and pipeline firepower make it a portfolio gem. Wait for a dip if you’re cautious, or ride the momentum if FOMO’s got you-either way, this pharma star’s got legs. Just don’t tell your broker you missed the boat because you were binge-watching instead of buying!

Or Donate:

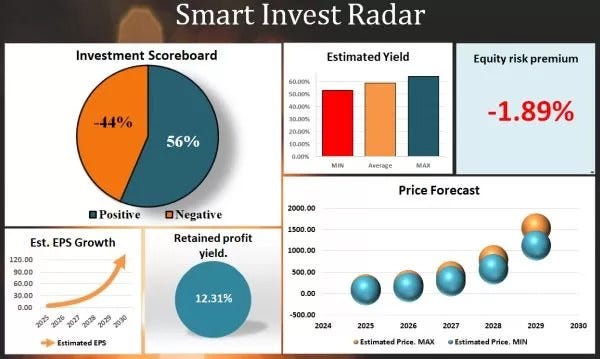

*Investment analysis involves scrutinizing over 50 different criteria to assess a company's ability to generate shareholder value. This comprehensive approach includes tracking revenue, profit, equity dynamics, dividend payments, cash flow, debt and financial management, stock price trends, bankruptcy risk, F-Score, and more. These metrics are consolidated into a straightforward Investment Scoreboard, which effectively helps predict future stock price movements.

**Use the price forecast to manage the risk of your investments.

Originally published at https://www.aipt.lt on September 19, 2025.

Why AbbVie ’s Stock Could Double by 2029: Grab It Before the Dip! was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.