Semiconductor stocks have moved from a powerful technology theme into one of the biggest drivers of U.S. equity market direction. The PHLX Semiconductor Sector Index, known as SOX, now accounts for a record 23% of the S&P 500’s market capitalization, according to fresh market data shared by The Kobeissi Letter.

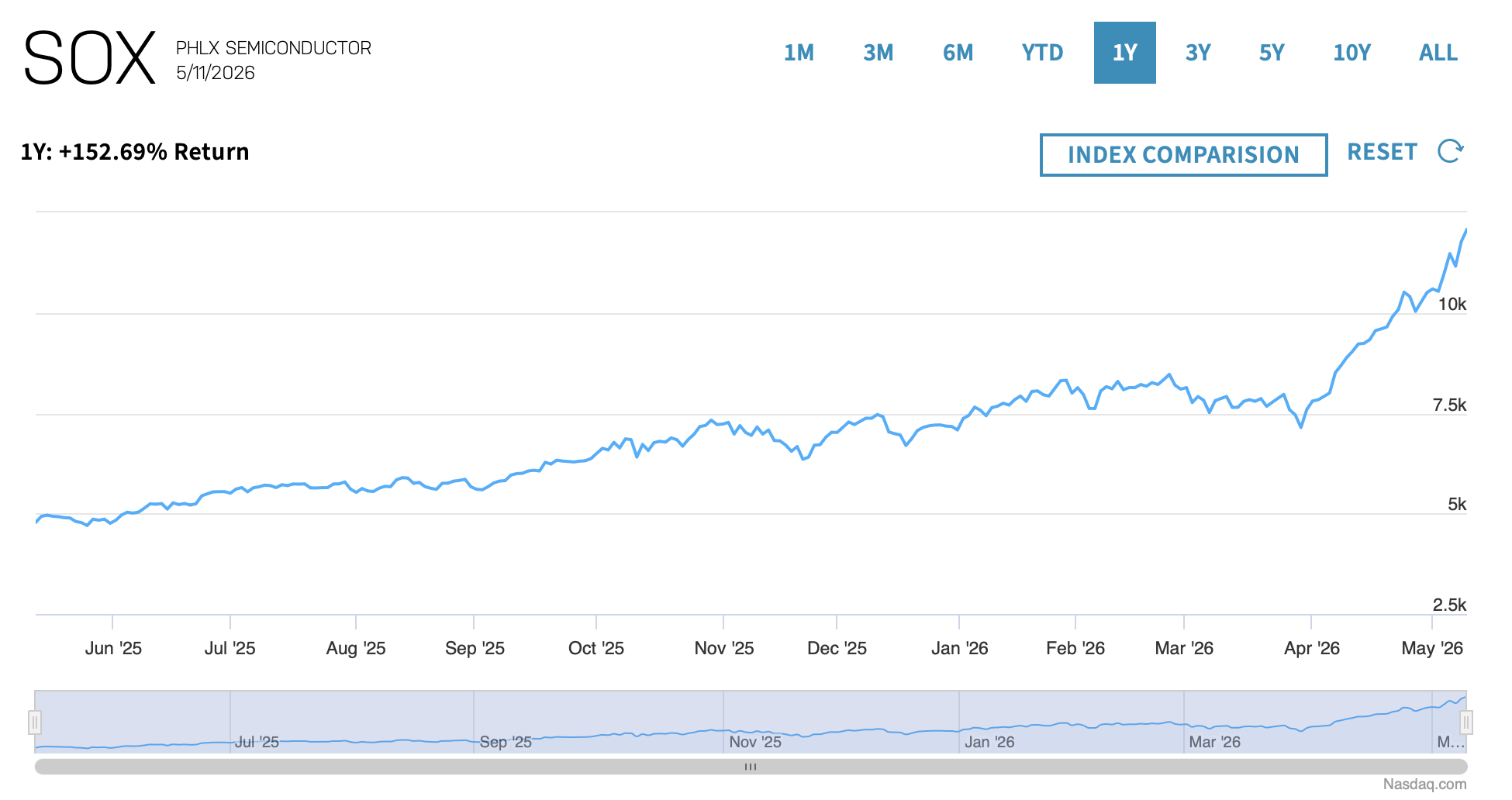

That share has doubled in two years, reflecting both the scale of the chip rally and the market’s growing dependence on artificial intelligence infrastructure. Over the same period, SOX has gained about 146%, far ahead of the S&P 500’s 43% advance. The move has turned semiconductor exposure into a central market factor rather than a narrow sector trade.

The PHLX Semiconductor Sector Index tracks 30 companies tied to the design, distribution, manufacture, and sale of semiconductors. It is a modified market capitalization-weighted index, which means the largest chip companies still carry heavy influence even though weighting rules limit excessive single-stock dominance.

That structure matters for market behavior. When chip leaders rise together, the effect reaches well beyond semiconductor ETFs or specialist portfolios. Passive funds, growth strategies, AI-linked baskets, and broad S&P 500 exposure can all become more sensitive to the same demand story: data centers, AI accelerators, memory, custom silicon, networking chips, and advanced manufacturing capacity.

The latest rally has been unusually persistent. SOX has finished higher in 24 of the last 28 trading days and has climbed about 65% over that stretch. Nasdaq’s latest index data placed SOX around 12,081, while FRED’s daily Nasdaq series showed the index at 11,775.50 on May 8, before the next leg higher.

The rally has also pushed SOX roughly 60% above its 200-day moving average, the widest gap since the dot-com era. In March 2000, the index traded about 110% above that long-term trend line before the semiconductor boom reversed into a sharp cycle reset. The current divergence is smaller than the 2000 extreme, but it still places chip momentum in historically stretched territory.

Broader market action has reinforced the concentration theme. U.S. stocks closed slightly higher on May 11, with the S&P 500 and Nasdaq reaching new record closing highs as semiconductors outperformed the wider market. Reuters noted that the PHLX Semiconductor Index jumped 2.6% in that session, while Intel and Qualcomm were among the major chip-related movers.

The rally is being powered by more than a single earnings beat or product cycle. Investors are pricing chips as the hardware layer behind AI infrastructure spending, cloud capacity expansion, memory demand, edge devices, and custom silicon partnerships. That gives the trade a stronger fundamental narrative than a purely speculative surge, but it also raises the cost of disappointment. A slowdown in AI capex, weaker chip orders, margin pressure, supply-chain friction, or a rotation out of crowded growth trades could have an outsized effect on the broader market.

The immediate risk is not simply that semiconductor stocks have risen quickly. The larger issue is market concentration. A sector that now represents a record slice of S&P 500 value can lift benchmarks when momentum is strong, but it can also amplify downside if stretched positioning meets weaker demand, higher rates, or profit-taking after a 65% run in fewer than 30 trading sessions.

The post Semiconductor Stocks Hit Record Market Weight As SOX Momentum Accelerates appeared first on Crypto Adventure.