Spot ETFs pulled the buyers into regulated markets. Perpetual futures pull in the leverage, the funding signal, and the cascades. And they showed up in a tightening tape, not an easing one.

Yesterday the CFTC cleared the first true bitcoin perpetual on a US-regulated exchange, and within a few hours the timeline had filed it next to the spot ETFs: another box checked, another reason to be long. That read is lazy. It’s also the read most people will act on, which is exactly why I want to take it apart.

The ETF approval was a demand story. It gave regulated capital a clean way to own spot bitcoin, and the flows showed up in the price. What cleared on May 29 is not a demand story. It’s a plumbing story, and the plumbing in question is the part of this market where price actually gets set and where leveraged accounts go to die.

The regime is tightening, and a regulatory headline doesn’t change that. The Fed has walked the market off its rate-cut expectations for the back half of 2026. The 30-year Treasury is sitting near 5.2%, the highest since 2007, and the 10-year is hovering around 4.6%. When the long bond pays you a real return to do nothing, a non-yielding asset has to fight for the marginal dollar, and right now it’s losing that fight.

The ETF flows show how institutions actually behaved into this. US spot bitcoin ETFs bled about $1.26B the week of May 18, most of it out of IBIT. That wasn’t a referendum on bitcoin. It was de-risking a non-yielding asset while real yields paid them to wait, the same trade that pulled money out of every long-duration position this spring.

That’s the tape the perp news landed in. Bitcoin is grinding in the high $70Ks, and the honest question for the past month has been whether the bid is macro sponsorship or just positioning holding the line. Into that, the US went and built a regulated on-ramp for leverage.

The most common error I’ve seen in the last 24 hours is treating Kalshi and Coinbase as the same event. They’re not, and the difference is the whole game.

Kalshi received an actual Order for Approval from the Commission to list BTCPERP, a no-expiry contract referencing bitcoin’s spot price, listed as a futures contract on a CFTC-designated contract market. That’s the real artifact. For the first time, a US regulator has put its name on a true perpetual, the same instrument that has run crypto’s offshore casinos for years. The contract tracks spot through a benchmark index and trades around the clock, with funding doing the work that an expiry date does on a normal future.

Coinbase did not get that. CFTC staff issued an interpretation and a no-action position to Coinbase Financial Markets, its registered futures commission merchant, covering a plan to route US customers into certain Deribit-listed contracts treated as foreign futures. The relief lets the firm post crypto and stablecoins as margin to a foreign broker, with those trades cleared through its Bermuda entity. In plain terms: Coinbase got a compliant hallway into offshore liquidity it already had a relationship with, not a homegrown product. Institutional onboarding starts now. Retail is “coming soon,” with options live first and perps behind them.

And the Commission was explicit that this is not a blanket yes. The companion policy statement limits the clean read to bitcoin and similarly deep, continuously traded digital commodities, and keeps everything else case-by-case. So no, “the CFTC approved crypto perps” is wrong. They approved one, and built a supervised door to a few more.

The distinction matters because one path manufactures new domestic liquidity and the other just reroutes existing offshore liquidity through a US-compliant pipe. On your screen, those look nothing alike.

If you only trade spot, you’ve been watching the small table.

Reuters, citing CryptoQuant, put perpetual futures volume at $61.7T for 2025. Other counts run higher; you’ll see $86T and $90T thrown around. The exact figure doesn’t matter, because the conclusion holds at any of them. Perps, not spot, are the dominant venue for crypto price discovery and the place leverage lives. The spot ETFs everyone fixates on sit on top of a market whose pricing engine has always been a perpetual contract on an exchange US regulators couldn’t see into.

A perpetual never expires, so it never forces the position-unwind a quarterly does. No roll, no settlement, no calendar. To keep it pinned to spot, longs and shorts pay each other a funding rate: when leverage skews long, longs pay shorts and the cost of staying long climbs; when it skews short, the reverse. That funding number is one of the cleanest positioning reads in the whole asset class. It shows you where the crowd is and who’s paying to stay there. When price turns, those are the accounts that get force-closed first.

The ETF crowd keeps missing this. ETF flows are a demand signal, and a lagging one. You find out where the money went after it already went there. Funding is real-time. It tells you, hour by hour, where the leverage is stacked and which side is about to get hurt.

For years that signal, and the cascades it produces, lived on Binance, Bybit, OKX, and Deribit. Offshore. Opaque to US oversight. Yesterday the CFTC started pulling that pricing-and-liquidation engine into its own jurisdiction.

Move leverage onshore and the funding rate stops being an offshore curiosity and becomes a regulated, visible number. That alone changes the institutional math. A US desk can finally run the basis trade, long spot against short perp to harvest funding, without booking exposure to a venue its compliance team won’t go near. Open interest starts accumulating inside CFTC-supervised venues, where margin and position limits actually bind. And the cascades, the ones that turn a 5% spot move into a 12% wick, start landing partly on rails a US regulator can watch.

That last piece is what the bulls are skipping. Onshoring leverage doesn’t sand down volatility. In the near term it can sharpen it, because you’ve added a new, lower-friction venue for leveraged exposure to a market that was already liquidation-driven. Regulated leverage is still leverage. A CFTC stamp doesn’t repeal funding risk, basis risk, or the arithmetic that turns a routine pullback into a margin call.

Now put it against the regime. You’re onshoring a leverage-and-funding engine into a tightening tape, where the dominant institutional flow is de-risking and real yields are fighting for every dollar. The melt-up version of this story needs easing liquidity underneath it: onshore leverage piles on top, price runs, funding goes deep positive, the carry feeds itself. That regime isn’t here. What’s here is a more efficient way to express leverage in a market with no liquidity tailwind to absorb it.

The offshore exchanges are the ones structurally short this. Binance, Bybit, and the rest captured crypto’s leverage flow for years because the US gave it nowhere else to go; the liquidity went offshore because Washington pushed it there. Selig has been open about wanting to reverse that, to pull both the flow and the firms back onshore. The CLARITY Act gave him the ground to stand on, and this is the agency using it. Strip out the cheerleading and yesterday wasn’t a gift to crypto. It was the CFTC reclaiming jurisdiction over a market that had been running beyond its reach, while this administration still has the appetite to back it.

The offshore venues won’t surrender that flow without a fight, and they hold the one card that decides everything: leverage.

The bear case isn’t that onshore leverage blows the market up. It’s that it doesn’t matter, because nobody uses it.

Offshore perps run up to 50:1. A CFTC-supervised venue won’t. The first US-regulated perp products are debuting with leverage well below the offshore norm, with real margin and gated access. Cap leverage low and the traders who actually move funding and open interest have no reason to leave Binance and Bybit. Worse leverage and more paperwork for the privilege of being onshore. The degens who set the funding rate aren’t optimizing for customer protection.

If that’s how it plays out, none of the structural shift I described happens. Kalshi’s BTCPERP becomes a thin, well-behaved product for compliance-bound desks. The Coinbase pipe into Deribit carries a trickle of institutional access. And the funding signal that matters stays where it’s always been: offshore, opaque, untouched. The CFTC will have paved a clean regulated road that the liquidity refuses to drive down.

That’s not a tail risk. It’s close to the base rate for regulated crypto venues competing against offshore leverage on price. The history here favors the casino.

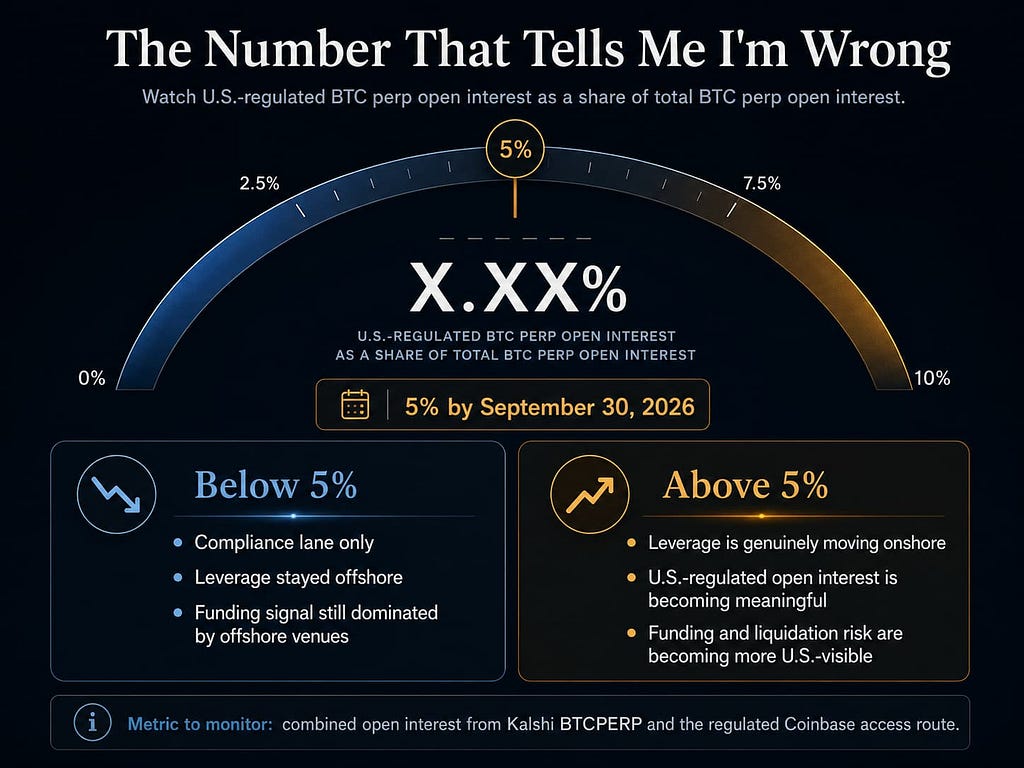

Here’s the line I’ll hold myself to. If combined open interest across the US-regulated perps, Kalshi’s BTCPERP plus whatever clears through the Coinbase pipe into Deribit, is still under roughly 5% of total bitcoin perp open interest by September 30, this onshored nothing. It built a compliance lane, the leverage stayed offshore, and the funding-comes-home thesis was wrong.

Clear that, and the engine has genuinely started to move, with everything that implies for how US-visible this market’s risk becomes.

The buyers came onshore with the ETFs. What came onshore yesterday is the leverage. In this regime that’s a reason to watch funding and open interest a lot more closely, not a reason to chase a green candle off a plumbing headline.

Originally published at https://cryptophiaresearch.com on May 30, 2026.

The CFTC Just Onshored Crypto’s Liquidation Engine — Cryptophia Research was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.