The British pound is maintaining a cautious tone following a period of elevated volatility, with market participants now focused on key upcoming UK economic data releases. Both GBP/USD and GBP/JPY are consolidating near important technical levels as investors await macroeconomic indicators that could provide clearer signals on the outlook for the UK economy and the Bank of England’s next policy moves.

The main event later this week will be the release of UK GDP data for April. Forecasts suggest the economy may contract by 0.1% month-on-month, following a 0.3% expansion in the previous month. At the same time, figures for industrial production, manufacturing output, construction activity, and the trade balance will also be published. Weaker-than-expected data could reinforce expectations of further Bank of England easing and put additional pressure on sterling, while stronger readings may support the currency and trigger a fresh wave of demand.

From a technical perspective, GBP/USD remains in a consolidation phase following its recent decline. After bouncing from support at 1.3300, a bullish piercing candlestick pattern formed on the daily chart, with potential follow-through towards 1.3420–1.3480. A sustained break below 1.3300, however, could extend the downside move towards the April lows in the 1.3220–1.3180 area.

Key events for GBP/USD:

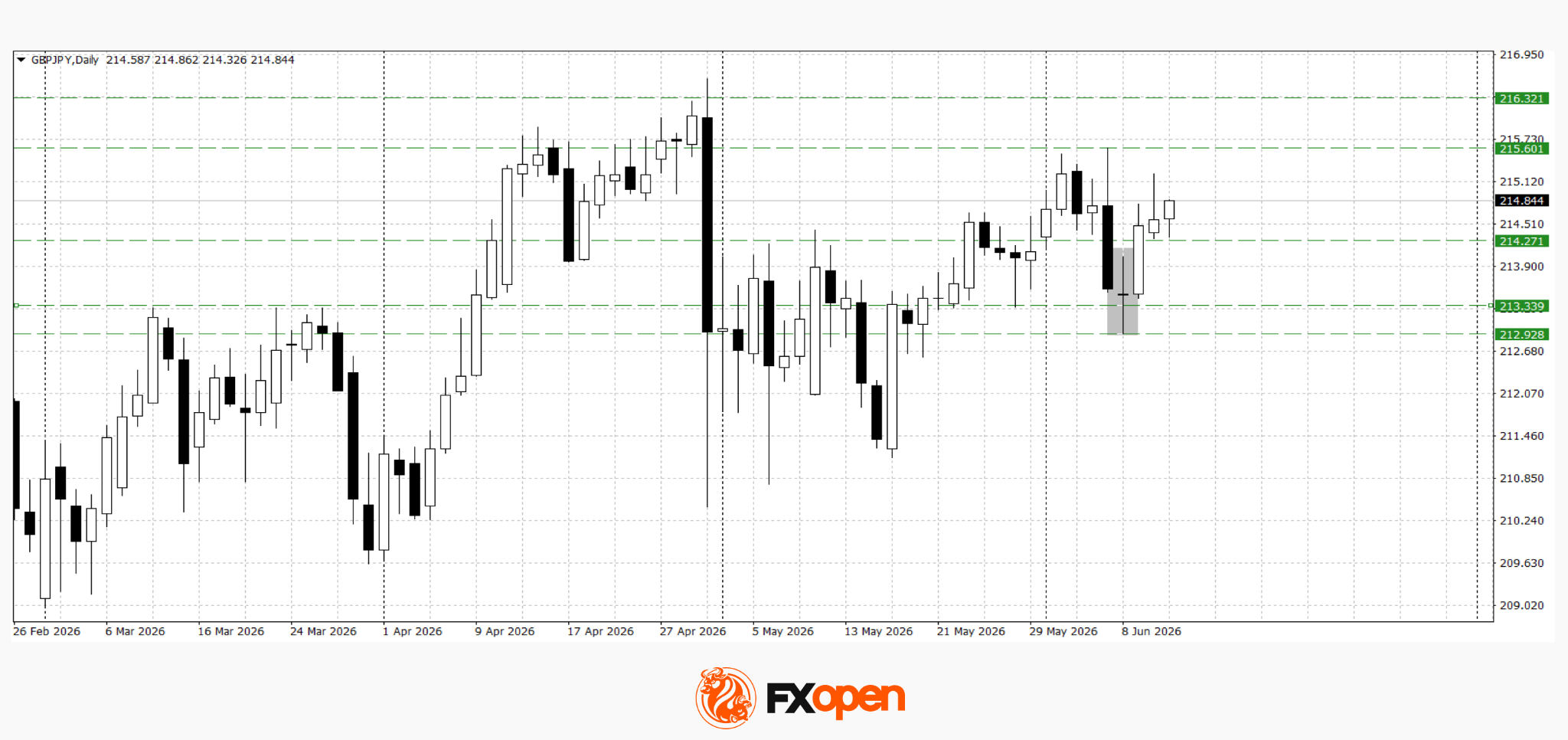

GBP/JPY is also trading in a consolidation range near important resistance levels. The pair continues to find support from persistent yen weakness, although the lack of a decisive breakout above recent highs suggests caution among buyers. Strong UK data could prompt another attempt to extend gains towards the 215.60–216.30 area. Conversely, a break below 214.20 may open the way towards 213.30–213.00.

Key events for GBP/JPY:

Overall, sterling is approaching a key juncture where its next direction will largely depend on the state of the UK economy. Upcoming GDP, industrial production, and trade balance data could act as the main short-term drivers for GBP/USD and GBP/JPY. Ahead of these releases, markets are likely to remain cautious, with consolidation near current levels remaining the dominant scenario.