Cards as a Service CaaS lets any software company issue and manage debit credit prepaid or virtual cards through APIs without building a bank or owning financial infrastructure

The model mirrors SaaS economics recurring platform fees plus usage linked revenue interchange turning payments into an ongoing revenue stream rather than a one time feature

Virtual card payments reached approximately 5.2 trillion dollars in 2025 with 76 percent driven by B2B transactions this is primarily a commercial payments story not consumer fintech hype

By 2025 70 percent of US corporations had adopted virtual cards up from 55 percent in 2022 The early adopter phase is over This is now infrastructure

The real value of CaaS is not issuing a card it is turning payments into a controllable software layer with built in data policy and monetization

The biggest misconception integration feels simple at the API layer The real complexity lives in reconciliation onboarding compliance and disputes and it never disappears It just shifts beneath the surface

Imagine you run a corporate travel platform Your customers book flights hotels and rental cars through your software Billions in annual spend flows through your ecosystem but none of it truly belongs to you It moves through banks card networks and issuing partners you do not control You see little of the data earn none of the interchange and have no control at the point of payment

Now flip that model

Within weeks you issue virtual cards to every traveler on your platform Each card is programmable spend limits merchant restrictions time windows tied to trips A hotel payment goes through your system in real time You see it instantly You earn on it And if something looks wrong you can freeze the card immediately

That is not theoretical anymore That is Cards as a Service

And it is why some of the most important innovation in fintech today is not happening in lending or crypto it is happening in who controls the payment layer inside software

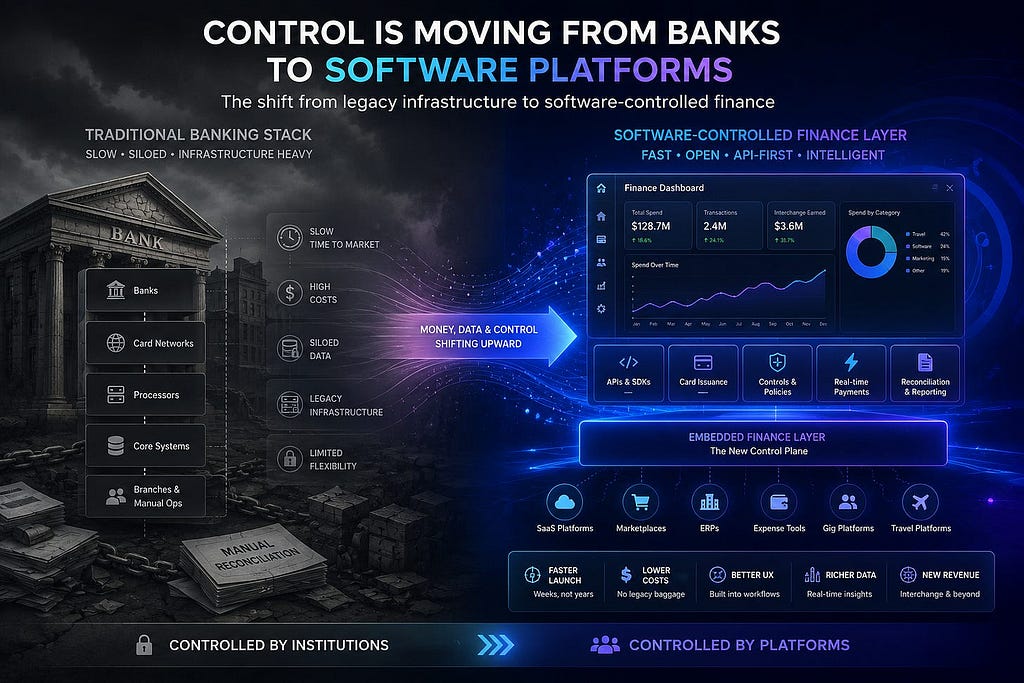

For most of software history payments were a dependency not a design choice You built the product banks handled the money

That separation made sense when becoming a payments company meant years of licensing compliance overhead network agreements and capital intensity

But it created a hidden cost Whoever controls payments controls three things software companies care about most user experience transaction data and monetization

If your platform processes 2 billion dollars in spend but routes it through someone else card program you have outsourced your most valuable financial layer

That equation is changing for two reasons

First card issuance has been abstracted into APIs much like infrastructure moved to AWS or CRM moved to Salesforce

Second embedded payments are structurally attractive Unlike subscriptions interchange is tied to usage Every transaction generates revenue It scales with customer activity not seat count

CaaS sits at the intersection of these forces It lets software companies behave like payments companies without becoming banks

The mechanics are straightforward though the simplicity is deceptive

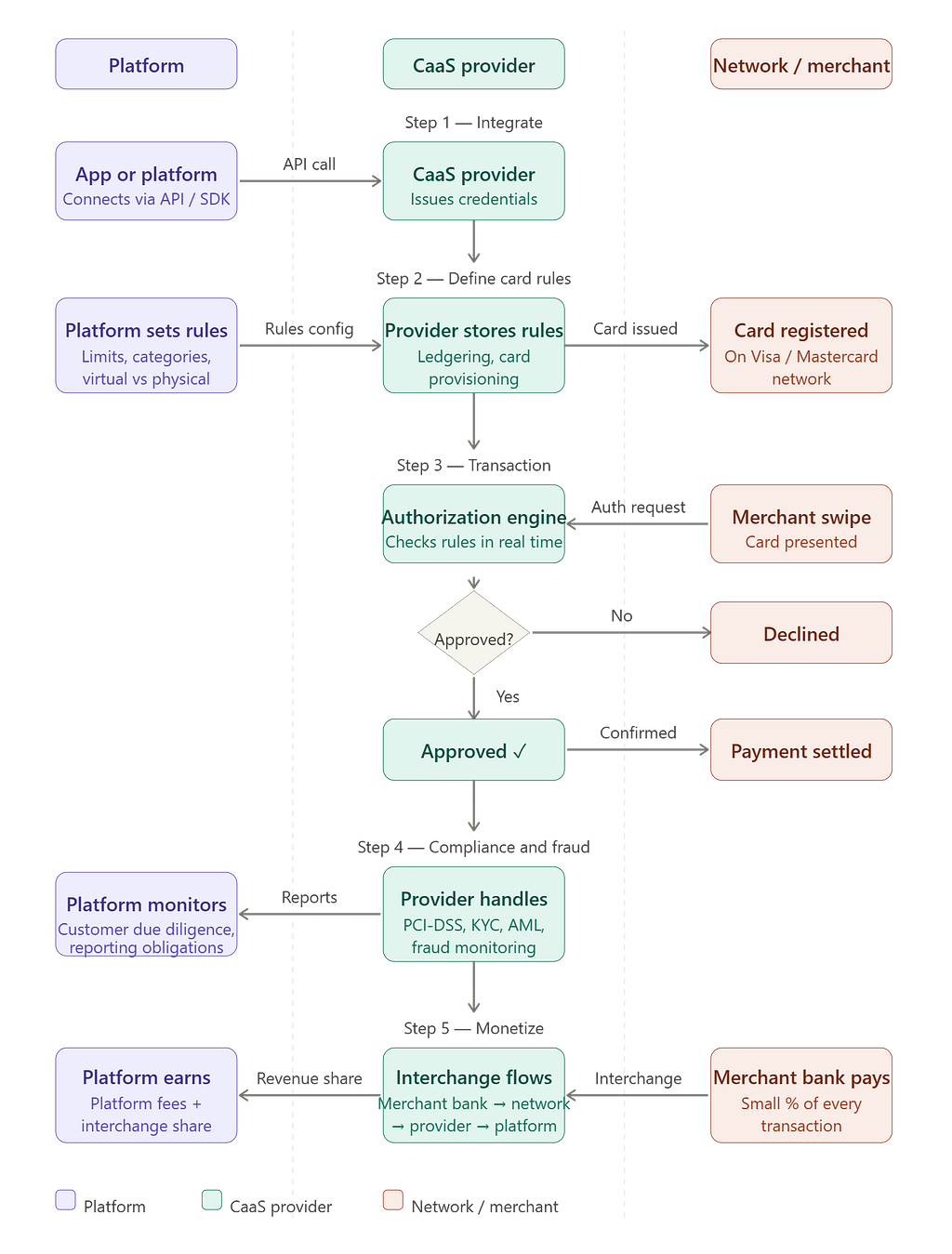

Step one choose a provider

Platforms like Paymentology Marqeta Galileo or Stripe Issuing provide the underlying banking relationships network access and compliance layer

Step two integrate via API

Modern onboarding feels like SaaS documentation SDKs sandbox testing and fast deployment

Step three define card behavior

Rules are configured programmatically spend caps merchant restrictions single use or recurring cards team level controls Enforcement happens in real time

Step four transaction execution

When a card is used the network routes the request The CaaS provider checks rules and fraud signals and responds in milliseconds Your systems do not touch the authorization logic

Step five monetization

Revenue comes from platform fees usage fees and interchange share the small cut from each transaction At scale this becomes meaningful recurring revenue

What makes this SaaS like is not the payment flow It is the revenue structure recurring base plus usage linked upside

SaaS wins on three fundamentals recurring revenue improving unit economics and switching costs CaaS mirrors all three and in some cases strengthens them

Recurring revenue

Unlike pure payment processing CaaS combines a fixed platform fee with transaction linked interchange You earn even when cards are not used and more when they are

Improving unit economics

As volume scales fixed infrastructure costs are amortized Compliance fraud and processing systems become more efficient per transaction

Switching costs

This is the real moat Once cards are embedded into expense systems procurement workflows or ERP logic they stop being cards and become infrastructure Replacing them means rebuilding workflows

Mastercard Paymentology and others frame it correctly this is not payment processing it is an embedded financial product

Virtual card payments reached approximately 5.2 trillion dollars in 2025, signaling that the scale is already institutional. Around 76 percent of this volume comes from B2B transactions, making it clear that this is primarily a commercial payments story rather than a consumer driven trend. Adoption has also reached maturity, with 70 percent of US corporations already using virtual cards, moving the market firmly into mainstream territory rather than early stage experimentation.

At the same time, the infrastructure behind issuance has compressed significantly, with launch timelines shrinking from years to weeks. This reflects a broader shift where payments infrastructure is becoming modular and API driven. Time to revenue has also improved by nearly 50 percent, enabling faster monetization cycles for platforms that embed card issuance into their products. Even small and medium businesses have increased card usage meaningfully, with average monthly spend rising from 10,000 dollars in 2020 to 23,000 dollars in 2025, reinforcing the idea that cards are no longer just a payment method but an operating layer within business workflows.

Taken together, these signals point to a clear conclusion. The infrastructure debate is effectively over. The real competition now is no longer about who can enable payments, but about who can control the layer on top of payments.

CaaS is powerful but not frictionless

Operational dependency

Your program depends on external infrastructure When it fails your brand takes the hit

Margin compression

Interchange is not stable It varies by region regulation and card type and is under long term pressure in many markets

Fraud and security

Even with advanced controls fraud risk persists And attribution risk often lands on the platform not the provider

Compliance

Regulation does not disappear it redistributes PCI AML KYC PSD2 responsibility is shared but never removed

The most overlooked risk is simpler APIs are easy Operations are not Reconciliation disputes and ledger accuracy are where complexity reappears after launch

Bull Case

Embedded finance becomes default Every workflow with payments integrates cards Platforms capture interchange they previously gave away Revenue scales with usage and switching costs deepen over time

Bear Case

Interchange compresses under regulation Large incumbents integrate vertically CaaS becomes commoditized infrastructure with thin margins unless scale is massive

Scenario A Workflow lock in works

Cards become inseparable from procurement or expense systems Spend scales with customers Interchange compounds into meaningful revenue

Scenario B Behavior does not change

Cards are issued but not adopted Users continue with existing payment methods Economics fail to materialize

Scenario C Regulatory compression

Interchange declines especially in regulated regions Revenue models break assumptions built on US economics

Scenario D ERP level adoption

Every invoice becomes a card transaction ERP systems embed payments natively This is where CaaS moves from product layer to financial backbone

Issuing a card is not the product

The product is the workflow that makes the card unavoidable controls policies automation and reconciliation

APIs hide complexity they do not remove it

The hard parts move downstream disputes compliance variation ledger integrity

Interchange is an outcome not a strategy

It only works when embedded into high frequency high value workflows Without that it does not scale

Spend frequency matters more than card issuance

Workflow depth determines switching cost

Geography reshapes economics dramatically

Commercial cards outperform consumer cards structurally

Provider concentration increases dependency risk

Compliance maturity determines long term survivability

CaaS is part of a larger structural shift the separation between software companies and financial services companies is dissolving

Financial infrastructure used to be gated by regulation capital and networks Now it is exposed through APIs

That changes competitive dynamics across banking expense management procurement and payouts

The biggest winners will not be card issuers They will be software companies that already sit inside high frequency payment workflows and decide to own the transaction layer instead of renting it

CaaS is not a fintech trend It is a restructuring of how software monetizes money flow

The SaaS analogy works because the economics are similar recurring revenue embedded workflows and increasing returns with scale

But the real shift is simpler payments are no longer a feature beneath software They are becoming part of the software itself

And in that shift the advantage goes to companies that understand one thing clearly you are not just issuing cards You are designing behavior

The most misunderstood part of embedded finance is the obsession with interchange

Interchange is not the business It is a byproduct of control over a workflow that already matters

The companies that succeed here do not start with payments They start with a real operational problem then realize payments are the most powerful way to shape behavior inside it

CaaS is just the tool

What matters is whether you use it to build infrastructure or just another feature

How CaaS Is Turning Payments Into a SaaS Business Model was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.