TL;DR:

Bitcoin is trading near $75,000 ahead of the month’s most significant options expiry: contracts worth approximately $7.9 billion expire this Friday on Deribit. Market positioning has turned this event into a determining factor for short-term price action.

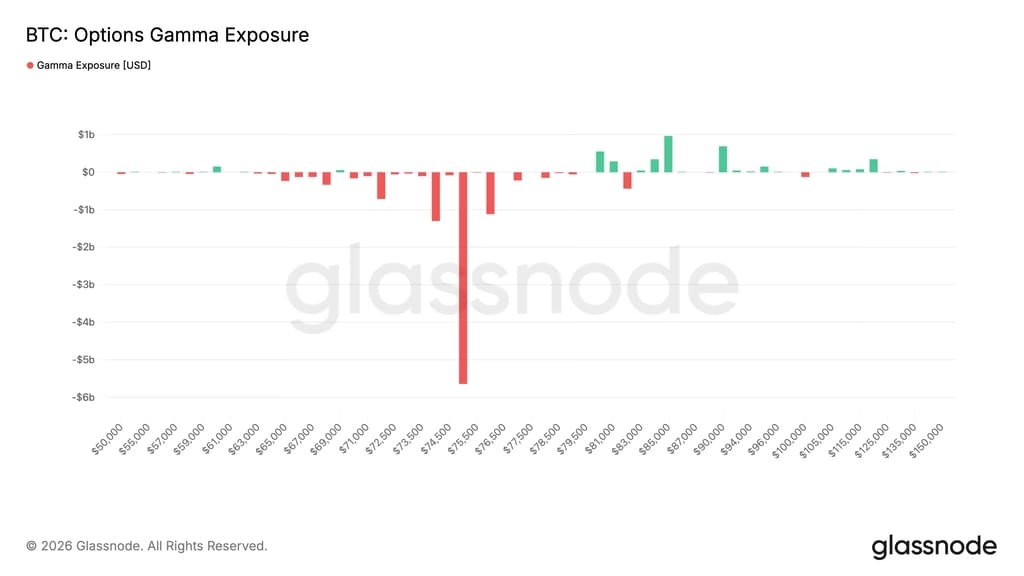

The highest concentration of open interest in calls —buy options, bullish bets— sits at the $75,000 strike, with around $395 million in active contracts, according to Glassnode. At that same level, gamma exposure is deeply negative, meaning dealer hedging flows tend to amplify price movements: if the price rises, they must buy more; if it falls, they sell more. The result is a zone of elevated volatility rather than stabilization.

On the bearish side, the highest concentration of puts sits at $62,000, with around $330 million in contracts. That level functions as the main downside protection zone. Between both extremes lies the “max pain” at $71,000, the price at which the greatest number of contracts would expire worthless, although this point can shift as price and open interest change ahead of expiry.

Unlike March, when Bitcoin was trading below max pain, the market is currently above that threshold. That puts Bitcoin’s ability to sustain recent gains to the test.

Funding rates in perpetual futures remain in negative territory, signaling an accumulation of short positions. If Bitcoin manages to hold firmly above $75,000, bearish traders could be forced to close their positions, generating additional upward pressure through a short squeeze.

Under that premise, Deribit’s weight in the options market becomes critically important. According to Checkonchain data, the platform holds around $31 billion in open interest, a figure that surpasses BlackRock’s IBIT ETF, which stands at around $28 billion, consolidating Deribit as the leading options market for crypto assets globally.