TL;DR:

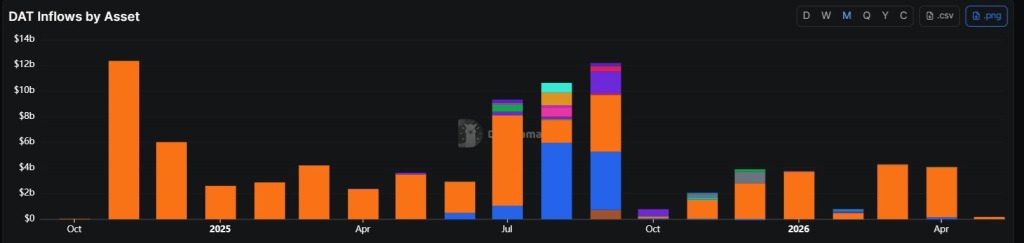

Digital asset treasuries posted their worst monthly result in more than seven months in May. According to data from DefiLlama, inflows into these companies reached just $180 million, a 95% drop compared to the $4.4 billion received in April and a 93% decline relative to the monthly average accumulated between January and May. The figures stand in sharp contrast with the two preceding months, during which the sector had taken in $4.2 billion in March and $4.4 billion in April.

Treasuries linked to Bitcoin concentrated virtually all of May’s inflows, with $177 million, equivalent to 98% of the monthly total. Yet even that figure resembles a freefall compared to the $3.8 billion that BTC-exposed firms had received in April. The rest of the ecosystem contributed only marginal amounts: ZCash, Story, and Sui recorded small inflows, while Litecoin posted a net outflow of $1.89 million.

Financial services firm Galaxy Digital was among the first to warn that the passive token accumulation cycle has come to an end. According to Galaxy, digital asset treasuries will need to put their assets to work through staking strategies, validator infrastructure, or decentralized finance models in order to continue justifying their existence to investors.

On May 26, staking infrastructure provider Everstake noted that Ethereum treasuries are already under pressure to generate active income, partly because cryptocurrency ETFs erode the appeal of companies that simply custody ETH. Among six firms that disclosed staking revenues, that activity represented on average 60% of their reported income.

Arthur Firstov, Chief Business Officer at payment infrastructure firm Mercuryo, argued that attributing the repricing of treasuries exclusively to ETFs “oversimplifies” the real dynamics of the market. Firstov noted that share dilution, operating costs, and balance sheet losses also weigh on the premiums or discounts at which these companies trade. “ETFs impose a structural constraint that did not previously exist. They establish a permanent ceiling on the premium that treasuries can charge,” he stated. Firstov added that staking improves capital efficiency in firms holding proof-of-stake assets, but that a yield of 3% to 5% cannot compensate for weak corporate structures or ongoing dilution.