Our Q3 Derivatives Report, “The Anchor and the Ceiling: Understanding the Structure of Funding Rates,” analysed the funding rate market, focusing exclusively on the structural forces that appear to influence it: the formula’s gravitational pull to the 0.01% baseline and the significant institutional capital that takes advantage of high funding rates. This revealed a bounded and often predictable environment, which is exactly the type of inefficiency that traders look to turn into consistent profit.

Understanding the fundamental mechanics is crucial, but the true challenge lies in applying to the trading desk. This article builds directly on our structural findings to provide a practical trading playbook on navigating funding futures as a novel trading instrument. It will cover everything from venue selection to executing funding futures trades on Boros.

Our previous report states that the funding rate formula is essential to anticipate the rate’s surprising behaviour in certain market conditions. Our analysis revealed that there is a gravitational zone defined by a structural floor and a capital-enforced ceiling.

The funding rate formula itself provides a powerful “floor.” Recall the formula: F = P + clamp(I – P, -0.05%, 0.05%), where I is 0.01%/8-hour for the exchanges in our analysis (BitMEX, Binance and Hyperliquid).

This formula inherently creates a positive bias. To illustrate, consider a scenario where sentiment is bearish and the perpetual trades at a discount to spot, with a premium (P) of -0.02%.

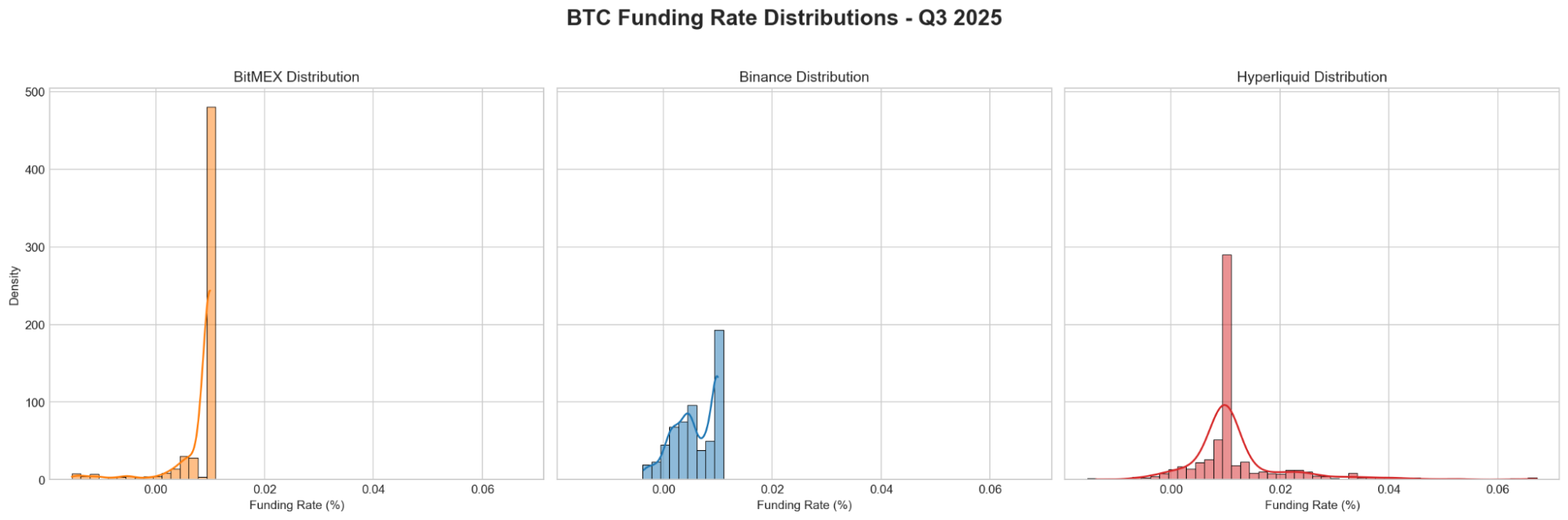

Even with the perpetual at a discount, the funding rate remains positive at its baseline. This mechanism provides a strong structural floor, explaining why funding rates for BTC are positive over 93% of the time in Q3 2025 on BitMEX, despite largely non-trending price action and a >10% drop towards the end of the quarter. A negative rate requires significant and sustained selling pressure to overcome this built-in positive drift.

If the formula provides the floor, institutional capital provides the ceiling. The baseline funding rate is annualised to 10.95% APY. This is roughly 100% more than the risk-free rate offered by USD money market funds, making it attractive for large players like Ethena. When premiums push the rate significantly above this level, it becomes a glaring opportunity for large-scale funding rate arbitrage.

Players like Ethena have billions of ready-to-deploy dollars to capture this delta-neutral yield by shorting the perpetual and buying the spot asset. This immense weight of capital acts as a hard ceiling, aggressively pushing any rate spikes back down toward the 0.01% anchor.

Together, the floor and ceiling create a predictable range, and significant deviations from this zone often represent trading opportunities.

Constructing Trade Idea Frameworks for Boros

Constructing Trade Idea Frameworks for Boros Understanding the structural floor and ceiling is the first step. The next is applying that knowledge to a trading venue. This requires a deeper look at the mechanics of Boros and a strategic framework that considers time, trading venue, and the implied rate.

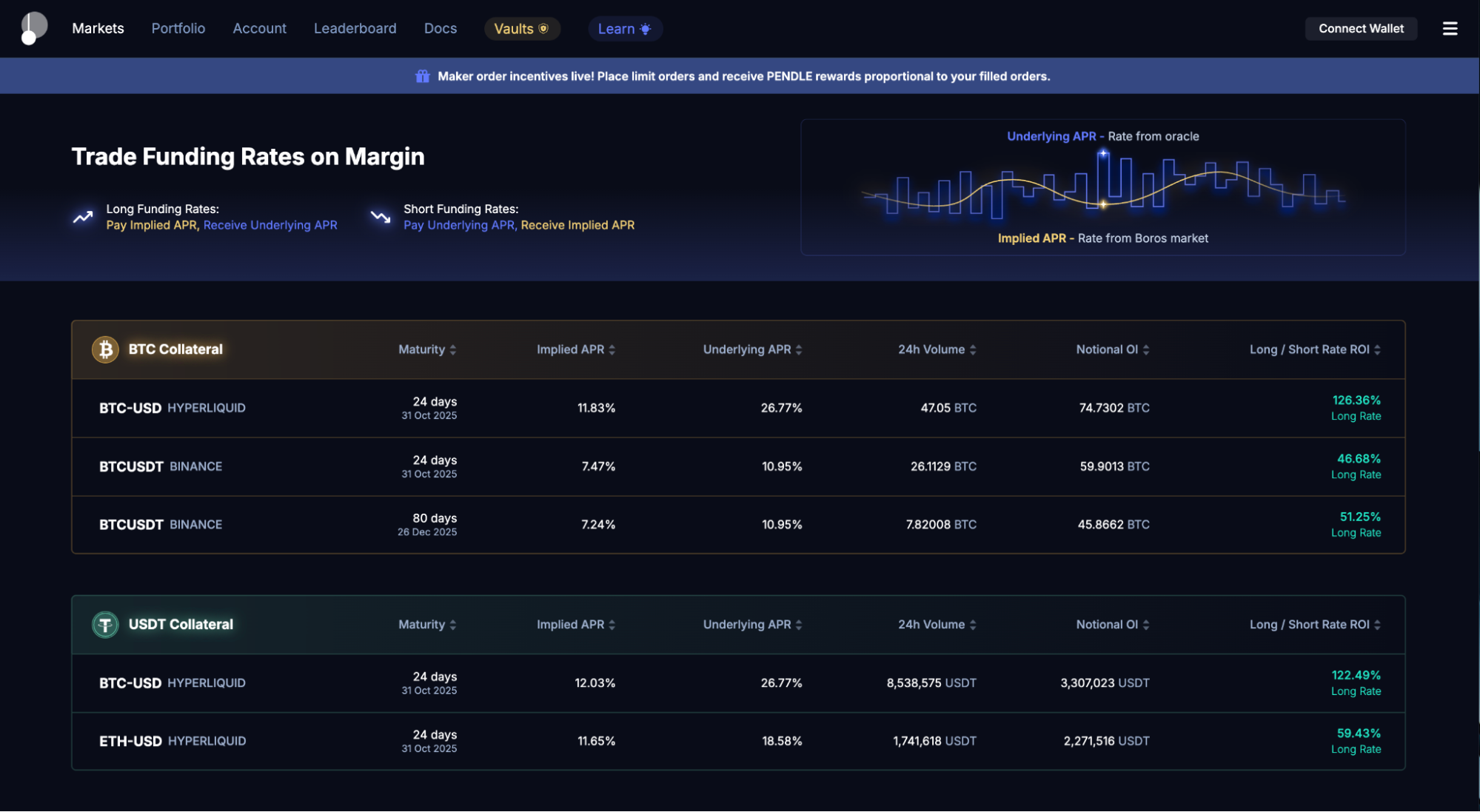

What is Boros?

Boros enables the trading of funding rates on-chain. With Boros markets, traders can hedge their funding rate exposure, as well as speculate on the volatility and movement of funding rates. With over 2.6 billion in volume less than 3 months since launch, it’s a nascent DeFi protocol with the potential to tap into a much larger perp market overall.

Understanding Boros’ Mechanics: Two Sources of Return

Trading on Boros is distinct from simply holding a perpetual swap. A trader’s profit or loss comes from two primary sources:

The Trading Strategy

A robust strategy considers three main variables: time, trading venue, and the entry point for the implied rate.

Variable 1 – Time (Expiration Matters): Every implied funding rate market on Boros has an expiration date. This is a critical factor in how sensitive the position is to short-term rate changes.

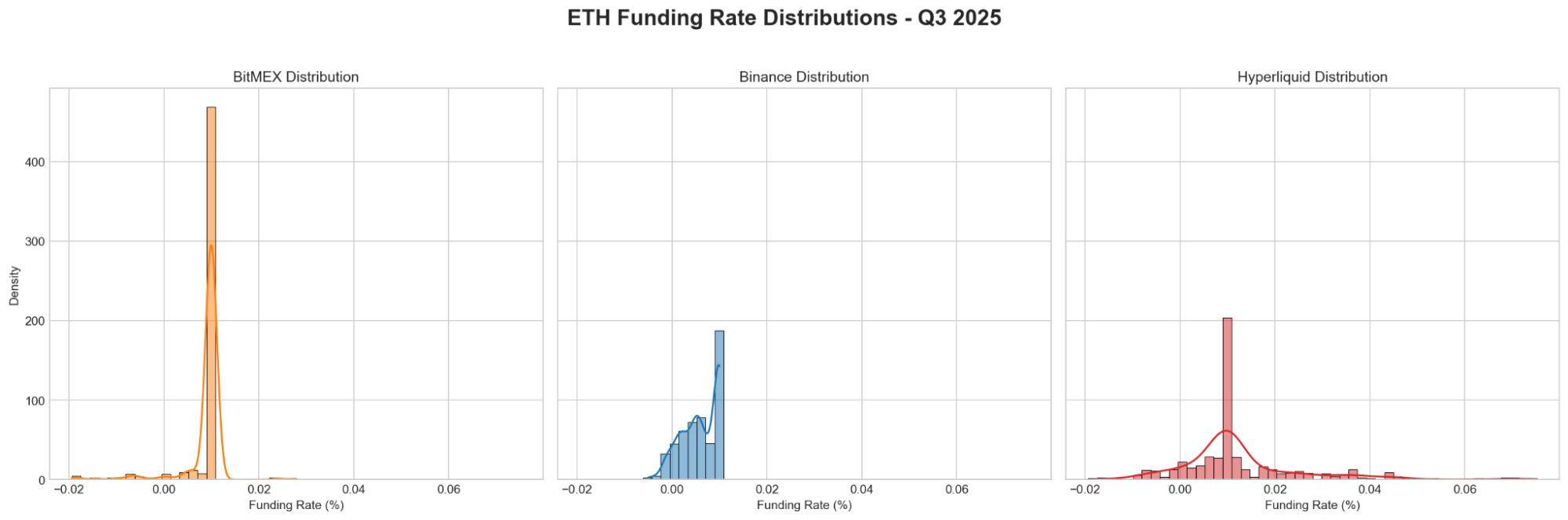

Variable 2 – Trading Venue (Choose Your Battlefield): As our previous report highlighted, the underlying venue dictates the rate’s behaviour.

|

Metric |

BitMEX (Stable) |

Hyperliquid (Volatile) |

Takeaway |

|

Mean Rate |

0.0090% |

0.0150% |

Hyperliquid carries a higher average premium. |

|

Std. Dev. |

0.0045% |

0.0250% |

Hyperliquid is nearly 6x more volatile, creating more trading opportunities. |

|

Min / Max |

-0.0194% / 0.0276% |

-0.05% / 0.10% |

The trading range on Hyperliquid is significantly wider on both ends. |

|

Freq. > 0.05%/8hr |

< 1% |

~15% |

Spikes offering high yield are far more common on Hyperliquid. |

Variable 3 – Implied Rate(A Scenario-Based Framework): With time and venue selected, the final decision is timing your entry based on the market’s implied rate relative to your expectation.

|

Scenario |

Trade |

|

1: Expecting an Overheated Market |

If you anticipate a period of bullish exuberance, funding rates are likely to trend higher. Trade: Long the implied rate when it’s below 10% APY. Justification: While the 10.95% anchor creates a powerful gravitational pull, periods of intense speculation can cause rates to temporarily overshoot this ceiling, offering an opportunity to capture both periodic payments and capital gains as the implied rate rises. |

|

2: Expecting a Neutral Market |

If you believe the market will be relatively balanced, significant deviations from 10.95% can be seen as opportunities.

Trade: Longing the implied rate if it drops significantly below this anchor, or shorting it if it rises too far above, betting on a reversion to the structural rate. Justification: The 10.95% APY acts as a structural anchor. Trading on deviations from this anchor allows for profit as the implied rate reverts to its structural mean. |

|

3: Expecting a Bearish Market |

If you anticipate bearish sentiment, remember the structural floor. The funding rate is still likely to remain positive due to the formula’s bias. This creates an asymmetric opportunity. Trade: Short the implied funding rate when it is relatively high (e.g., above 7% APY). Justification: The goal is not to bet on the rate going negative, but on it compressing from a high positive level towards its lower, structurally-supported floor (e.g., near 4% APY). |

The following steps provide a general framework for implementing a strategy based on the concepts discussed.

Step 1: Formulate a Thesis

Before placing any trade, establish a clear thesis based on the structural framework. Are you expecting a reversion to the mean, a spike due to market exuberance, or a compression towards the structural floor?

For example, a thesis could be: “The implied rate on Hyperliquid is currently elevated due to short-term FOMO, and I expect it to compress back towards its structural anchor.”

Step 2: Select Your Market and Expiration

Based on your thesis, choose the appropriate trading instruments:

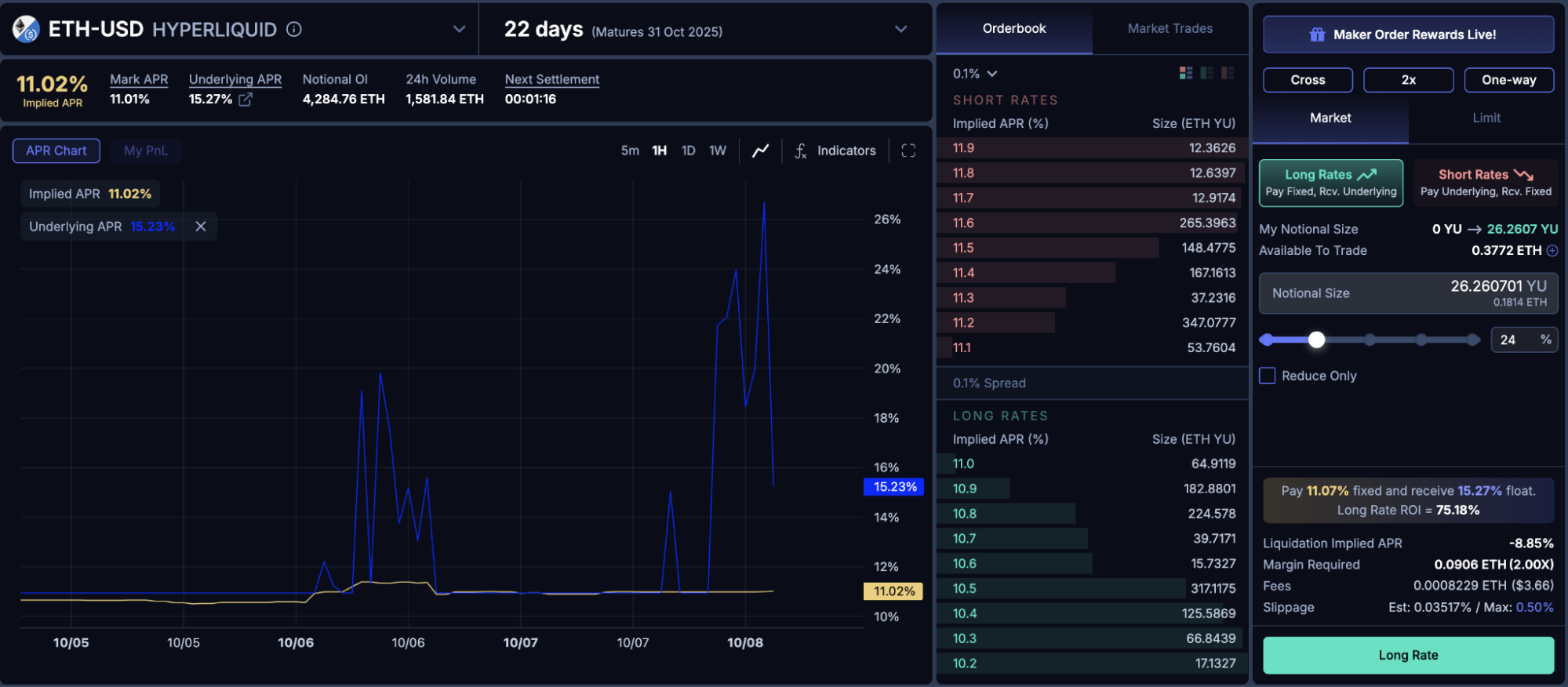

Step 3: Execute the Trade on the Order Book

Step 3: Execute the Trade on the Order Book

Navigate to the Boros platform and connect your wallet. Based on your thesis, you will either long or short the implied funding rate.

Navigate to the Boros platform and connect your wallet. Based on your thesis, you will either long or short the implied funding rate.

Step 4: Monitor and Manage Your Position

Once your order is filled, actively manage the position by monitoring the two sources of return:

Step 5: Exit the Strategy

You can realise your profit or loss in two primary ways:

The ability to trade funding rates directly marks a significant evolution in crypto derivatives. Our analysis suggests that success in this new arena may come less from predicting market sentiment and more from understanding market structure.

By recognising the structural floor created by the funding formula and the hard ceiling enforced by arbitrage capital, traders can build a robust framework. The playbook is no longer about guessing market direction but about identifying when the market is deviating from its own structural norms. By systematically fading unsustainable premiums or buying into fear-driven dips toward the structural floor, traders can begin to master the new, more predictable world of funding rate derivatives.

The post The Boros Blueprint: How to Trade Funding Rates appeared first on BitMEX Blog.