Micron Technology prepares to report fourth-quarter fiscal 2025 results on Tuesday, September 23, after market close. The memory chipmaker has seen its stock surge more than 93% year-to-date as investors bet on artificial intelligence demand.

Wall Street analysts expect strong numbers from the Boise-based company. Consensus estimates call for adjusted earnings per share of $2.81, representing 138% year-over-year growth. Revenue projections sit at $11.12 billion, marking a 43% increase from the prior year period.

The company has a solid track record of beating expectations. Micron has exceeded consensus earnings estimates for nine straight quarters. Last month, management raised its own guidance for the fourth quarter.

Company executives now project revenue of $11.2 billion, give or take $100 million. They also expect adjusted earnings per share of $2.85, plus or minus seven cents. The guidance increase came after improved pricing in DRAM memory chips and solid execution across business units.

Several Wall Street firms have raised their price targets ahead of earnings. Rosenblatt analyst Hans Mosesmann maintained his Buy rating with a $200 price target. The analyst expects a modest beat relative to the company’s August guidance update.

Mosesmann sees stronger upside potential for the November quarter outlook. He points to constrained DRAM and NAND Flash wafer supply through 2026. Accelerating demand from AI workloads supports his bullish view.

The analyst believes DRAM demand has already exceeded available supply. He calls Micron his “top long idea as the memory up-cycle accelerates into FY26.” AI systems require vast data storage capabilities, fueling strength in storage markets.

TD Cowen analyst Krish Sankar raised his price target to $180 from $150. He maintained a Buy rating on the stock. Sankar expects continued outperformance in the short term as momentum indicators remain positive.

The analyst sees potential for November earnings guidance to beat Street estimates by about 15%. He focuses on whether high-bandwidth memory pricing gets locked in for calendar 2026. Average selling price trends become more important at this cycle stage.

Mizuho provided the most recent analyst action, raising its price target to $182 from $155 on September 16. The firm maintained an Outperform rating ahead of the September 23 earnings report. Analysts anticipate accelerated high-bandwidth memory demand.

They forecast higher sales of HBM3e memory chips. Nvidia’s new GB300 chips are driving stronger orders from customers. The firm estimates 25% of Nvidia’s July-quarter shipments were GB300 versus GB200 chips.

GB300 mix could exceed 50% in the October quarter. This shift may provide upside for Micron’s November quarter guidance. The faster adoption of newer chip architectures benefits memory suppliers.

TipRanks‘ AI Analyst assigned an Outperform rating with a $137 price target. The AI analysis highlights solid financial performance and positive earnings call insights. Technical analysis supports a bullish outlook, though overbought conditions warrant caution.

Options traders expect volatility around the earnings announcement. Using at-the-money straddle calculations, the expected move sits at 10.3% in either direction. This reflects the market’s anticipation of a material stock reaction.

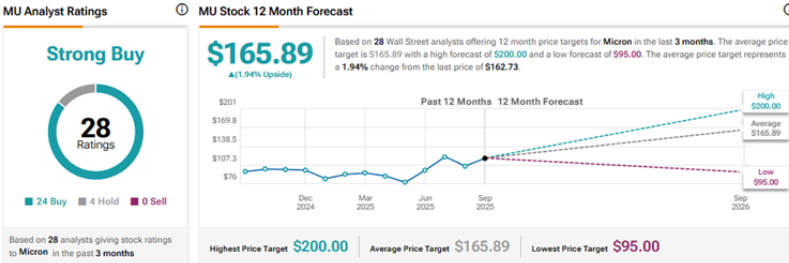

Wall Street maintains a Strong Buy consensus rating on Micron stock. The rating combines 24 Buy recommendations with four Hold ratings. The average price target of $165.89 suggests modest 2% upside potential from current levels.

The post Micron (MU) Stock: Analysts Boost Price Targets Before Q4 Earnings. Time To Buy? appeared first on CoinCentral.