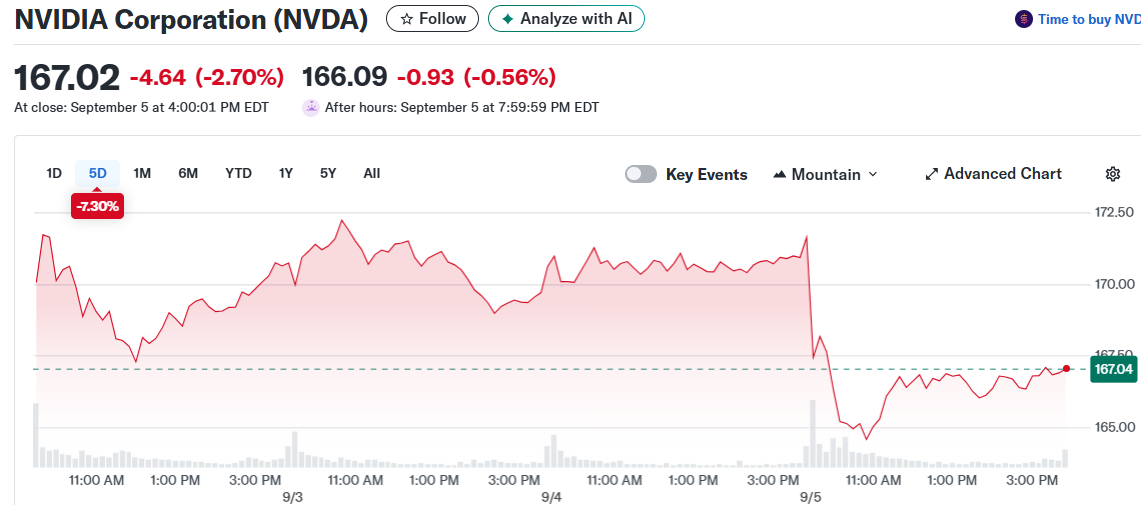

Nvidia shares bounced back Thursday after nearly completing a sixth straight losing session. The stock remains down 7% from its September peak despite recent recovery efforts.

Tech analyst Beth Kindig believes Wall Street is missing the bigger picture. She argues investors are focusing too much on lackluster second-quarter results instead of the underlying growth drivers.

“If this was just based on Q2, this stock would sell off much more than what it did,” Kindig told the Wealthion podcast. She points to a surge in networking revenue as a key indicator of future performance.

The networking revenue growth provides important clues about next-generation GPU systems. These new systems require much more networking capability than current generation chips.

Kindig dismisses concerns about China as overblown. The next-generation Blackwell chips are estimated to generate $100 billion in annual sales compared to just $15 billion from China.

Nvidia has evolved beyond just making chips, according to Kindig’s analysis. The company now integrates hardware, networking and software into powerful interconnected systems.

She compares this transformation to Apple’s dominance with the iPhone, iOS and App Store ecosystem. The value lies in the complete integrated solution rather than individual components.

Kindig’s projections far exceed current Wall Street estimates. She expects Nvidia to reach $75 billion quarterly from data centers by end of 2026.

Her forecast calls for $500 billion in annual data center revenue by 2028. This compares to the Visible Alpha analyst estimate of $293 billion for fiscal 2028.

CEO Jensen Huang previously mentioned a 50% compound annual growth rate for the AI market. Kindig uses this metric to support her aggressive revenue projections.

“If we get to a $500 billion data center segment by 2028, we’re at roughly $200 billion now,” she explains. This would imply roughly 100% room for stock price appreciation.

Broadcom’s third-quarter results provide additional validation for the AI growth story. The company reported record revenue of $15.95 billion, up 22% year-over-year.

AI-focused revenue jumped 63% to $5.2 billion, marking the tenth consecutive quarter of AI-driven growth. Free cash flow increased 47% to $7 billion.

Broadcom CEO Hock Tan revealed a new hyperscale customer had qualified for custom AI accelerator production. This expanded the company’s customer base beyond its existing three major clients.

The combination of higher demand and new customers pushed Broadcom’s backlog to $110 billion. This represents a substantial increase from previous quarters.

Tan raised fourth-quarter guidance to $17.4 billion in revenue, representing 24% growth. The guidance exceeded analyst expectations of $17.01 billion.

The CEO indicated 2026 growth could accelerate beyond originally planned levels. He also received a contract extension until at least 2030 from the board of directors.

Big tech companies remain in an arms race for improved AI technology. Even if current buyers slow spending, large enterprises previously shut out may enter the market.

Energy consumption presents the main challenge going forward. Systems using Rubin and Rubin Ultra chips will require 3 to 5 times more power than current technology.

Broadcom’s results confirm that hyperscale customers are increasing capital expenditures beyond previously announced levels. This trend directly benefits Nvidia as the dominant GPU supplier with 92% market share.

Nvidia currently trades at 27 times next year’s expected earnings despite recent stock gains of over 1,070% since early 2023.

The post Nvidia Corp (NVDA) Stock: Analyst Predicts 100% Upside as AI Demand Accelerates appeared first on CoinCentral.