SK Hynix (HXSCL) has been doing the investor relations rounds, and the message coming back is loud and clear: Wall Street likes what it’s hearing.

The South Korean memory chipmaker told investors this week that it received “tremendously positive” feedback on its plans to list in the US. The company filed a confidential application with the SEC back in March, with reports suggesting it could raise up to $14 billion.

The company noted it cannot give specific updates while the SEC review is ongoing. It confirmed it plans to issue ADRs within 2026, though the size and timing have not yet been decided.

SK Hynix’s pitch to investors is built largely on its position in the AI hardware supply chain. The company is a key supplier of high-bandwidth memory, or HBM chips, to Nvidia (NVDA). It competes in that space with Samsung Electronics (SSNLF) and Micron Technology (MU).

On HBM pricing, the company told investors it expects favorable conditions to carry into next year. Talks with customers on future pricing of these advanced chips — used in AI accelerators — are still ongoing.

There’s another angle worth watching. SK Hynix flagged strong demand for LPDDR memory — the low-power chips typically found in phones and tablets — from Nvidia for its next-generation Vera Rubin AI platform.

The company said this demand could tighten supply across the broader memory market from 2027. To get ahead of that, SK Hynix said it plans to adjust investments and product mix to maximize output.

That said, the company was straight with investors: it can’t guarantee it will be able to fully meet all demand, as expectations point to demand outpacing supply.

The Korean-listed stock (000660.KS) has had a run worth noticing. Over the past month, it’s up 58.2%. Over the past year, the gains are described as multifold — the kind of move that raises fair questions about what’s already priced in.

Despite the rally, valuation analysis from Simply Wall St gives the stock a valuation score of 5 out of 6, with a DCF model putting the intrinsic value at approximately ₩4,344,339 per share. That implies the current price sits at a 47.3% discount to that estimate.

On a price-to-earnings basis, SK Hynix trades at 21.58x. The semiconductor industry average sits at 24.42x, and a peer group average comes in at 71.00x. Simply Wall St’s proprietary Fair Ratio estimate for SK Hynix is 67.69x — well above where the stock currently trades.

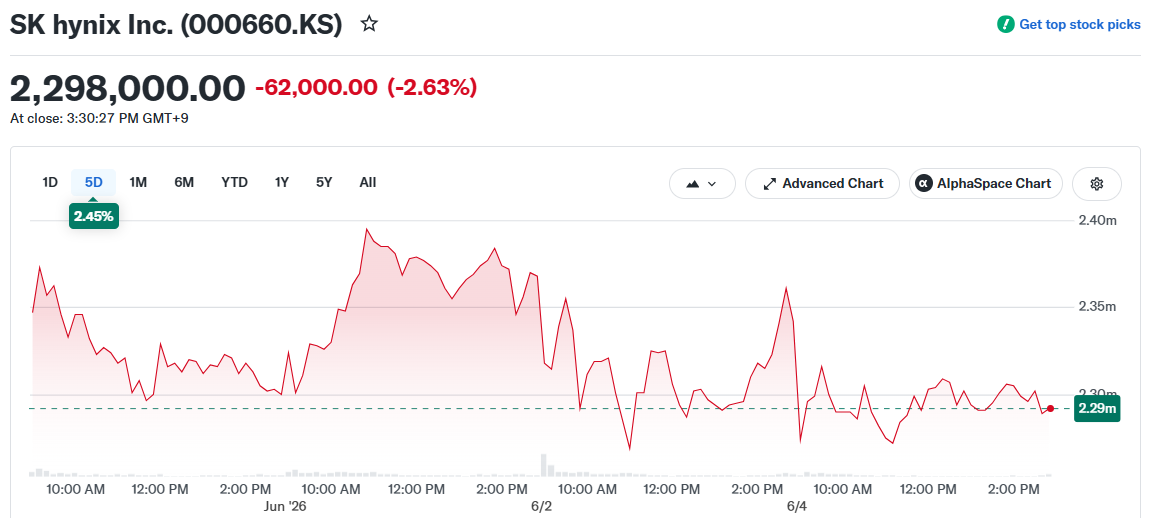

The HXSCL ADR was down slightly in recent trading, reflecting the broader Korean market session where 000660.KS slipped 2.63%.

SK Hynix last traded at those levels as the SEC review of its US listing application continues, with no confirmed timeline on when a decision or launch could come.

The post SK Hynix Stock: US Listing Gets “Tremendously Positive” Feedback as AI Demand Drives Momentum appeared first on CoinCentral.