The U.S. dollar is heading for its worst weekly performance in nearly three months after a disappointing June jobs report threw cold water on expectations for a Federal Reserve rate hike.

Nonfarm payrolls grew by just 57,000 in June. That was far short of the 110,000 economists had forecast. Payroll figures for the prior two months were also revised lower.

The labor force participation rate fell to 61.5%, its lowest level in more than five years. Traders quickly reassessed how likely the Fed is to raise rates in the near term.

BREAKING: The US economy adds 57,000 jobs in June, well below expectations of 114,000.

The unemployment rate fell to 4.2%, below expectations of 4.3%.

May's jobs number was also revised down by -43,000 jobs.

The labor market remains in a volatile situation.

— The Kobeissi Letter (@KobeissiLetter) July 2, 2026

Markets had been pricing in roughly a 64% chance of a September hike before the data dropped. That number fell to somewhere between 35% and 52% depending on the measure, according to CME FedWatch and LSEG data.

U.S. Treasury yields also pulled back. Two-year note yields, which are sensitive to rate expectations, snapped a three-day winning streak with a four basis-point drop.

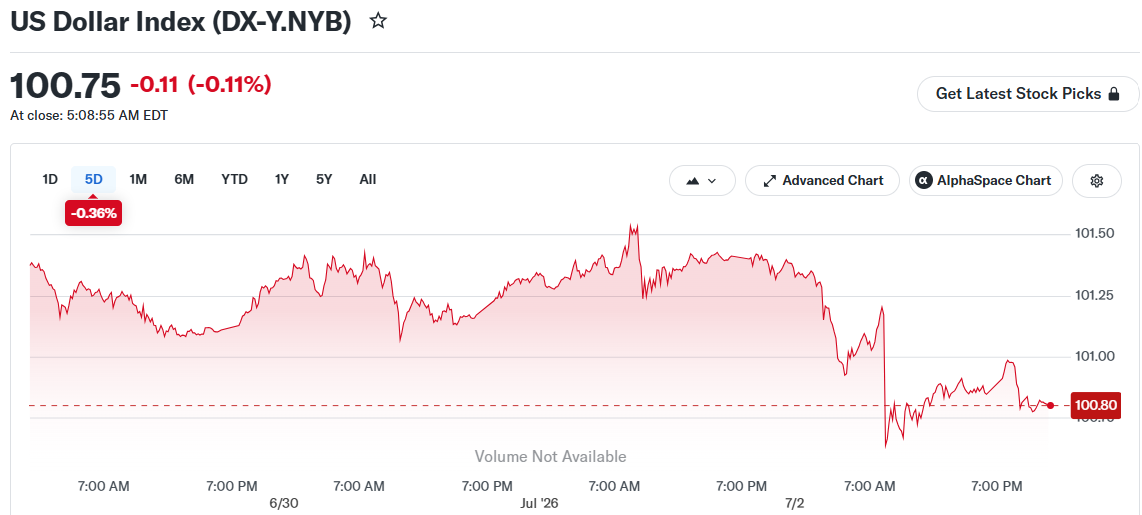

The dollar index, which tracks the greenback against a basket of major currencies, fell around 0.3% to 100.68 on Friday. It is now down about 0.7% for the week, the biggest weekly decline since early April.

The euro climbed to near $1.1472, close to a two-week high, and is up around 0.6% for the week. The British pound strengthened to $1.3380, on track for a weekly gain of 1.2% — its best in almost three months.

The Australian dollar rose to $0.6935, set to snap a four-week losing streak. The New Zealand dollar gained about 1.2% for the week.

Karl Steiner, head of analysis at SEB, said the weak data was in line with his team’s view that the dollar would eventually turn lower. He said more downside was possible.

The Japanese yen got some breathing room this week, pulling back above 161 per dollar after hitting a 40-year low of 162.84 on Thursday.

Japan’s Finance Minister Satsuki Katayama said on Friday that Tokyo is in regular contact with Washington on foreign exchange and stands ready to act. Chief Cabinet Secretary Minoru Kihara said officials were monitoring markets with urgency.

Investors are now watching for possible intervention, especially during thin holiday trading with U.S. markets closed for Independence Day.

Analyst Tony Sycamore at IG said 162.83 looks like a short-term top for dollar-yen. He said where the pair goes next will depend largely on upcoming U.S. economic data and moves in the Japanese government bond market.

The post U.S. Dollar Heads for Biggest Weekly Drop in 12 Weeks After Weak Jobs Report appeared first on CoinCentral.