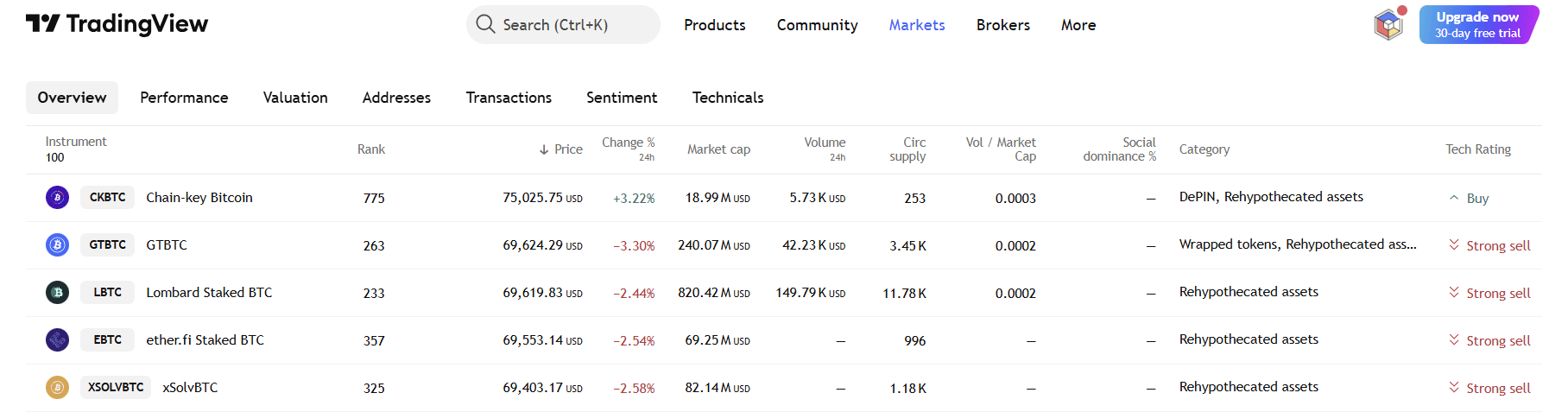

At first glance, tokens like LBTC, ckBTC, or staked BTC may look like new versions of Bitcoin. But in reality, they are financial layers built on top of Bitcoin, not Bitcoin itself.

Wrapped and staked BTC are derivative assets that represent Bitcoin in different environments:

These tokens typically aim to maintain a 1:1 value with BTC, but they come with very different mechanics and risks.

Understanding the differences is key before interacting with any of these assets.

👉 Example use: Providing liquidity on Ethereum-based platforms

👉 Example use: Earning passive returns on BTC holdings

👉 Example use: Trading exposure without owning BTC

One of the most overlooked concepts in crypto today is rehypothecation.

This means the same Bitcoin can be used multiple times across different platforms.

Here’s a simplified example:

1 BTC is locked in a protocol

→ A wrapped token is issued

→ That token is used as collateral

→ Another asset is created from it

Now, multiple claims exist on the same BTC.

This creates what many call:

👉 “paper Bitcoin” inside DeFi

Despite not being real BTC, these assets trade close to Bitcoin’s price because:

However, small deviations can occur due to:

This is where things get serious—and often misunderstood.

If the entity holding the BTC fails, the token may lose its backing.

Bugs or exploits in DeFi protocols can lead to loss of funds.

The token may lose its 1:1 value with BTC during market stress.

Some of these tokens have very low volume, making them hard to exit.

The rise of wrapped and staked BTC is not random—it’s driven by major shifts in the crypto market:

Bitcoin is no longer just a store of value—it is becoming programmable capital.

It depends on your strategy.

While wrapped and staked BTC open new opportunities, they also introduce layers of complexity and risk.

Owning Bitcoin directly is fundamentally different from holding a representation of it.

As the ecosystem evolves, one key question remains:

👉 Is your Bitcoin truly Bitcoin—or just a claim on it?