| Category | Assessment |

|---|---|

| Product Type | Crypto launchpad, staking platform, airdrop hub, farms, and vaults |

| Native Token | DAO |

| Main Use Case | Launchpad access, staking, allocation power, and early-stage project participation |

| Strongest Feature | Long operating history, large user base, and active launchpad infrastructure |

| Main Weakness | DAO trades like a low-liquidity small-cap token despite the platform’s history |

| Best Fit | Users who understand early-stage launchpad risk and want allocation access through staking |

| Risk Level | High |

| Editorial Score | 7.3/10 |

DAO Maker is a crypto launchpad and startup growth platform built around early-stage token access. It gives blockchain projects a way to raise capital and build communities, while users can participate in launches, airdrops, farms, vaults, and staking products through the DAO Maker app.

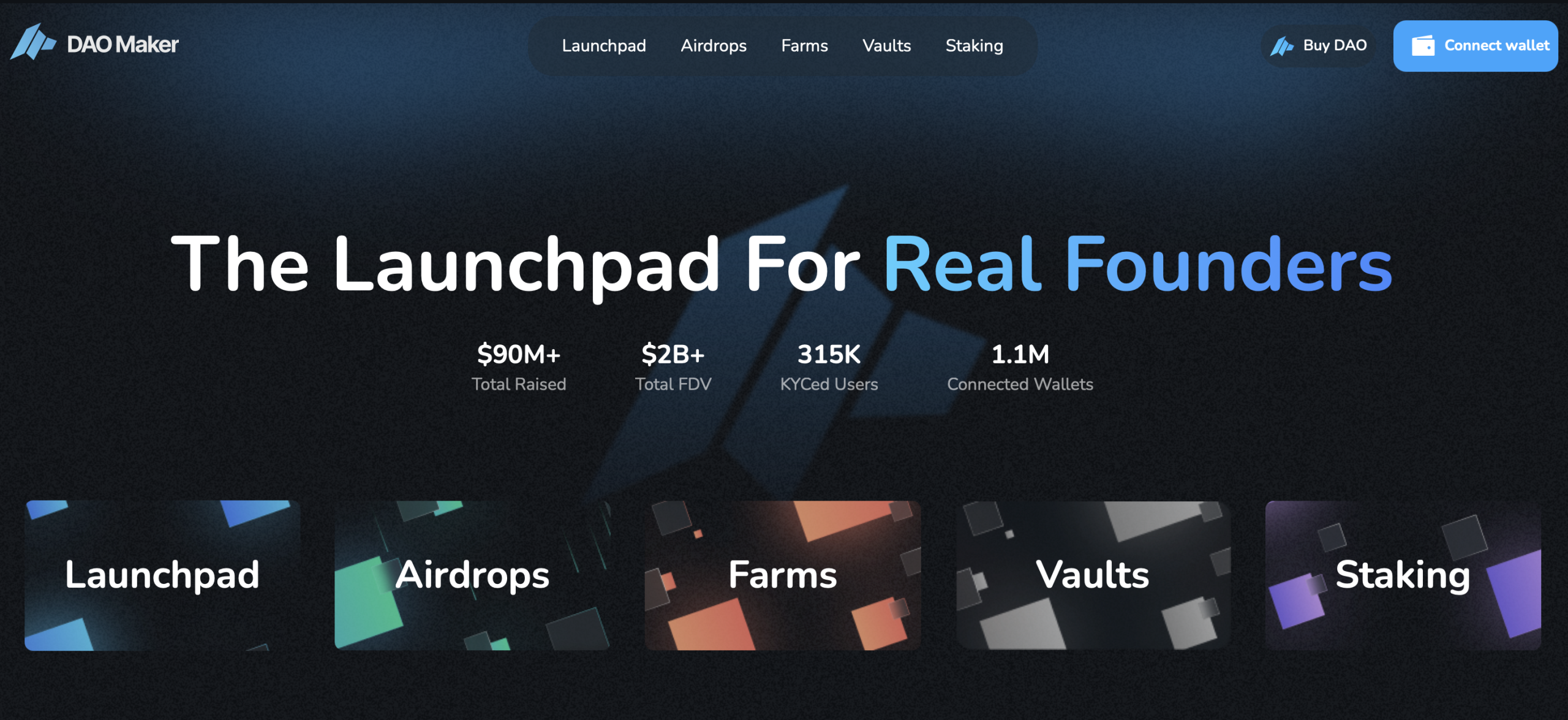

The platform’s current positioning is built around scale. DAO Maker has processed more than $90 million in total raised value, over $2 billion in total FDV across supported launches, more than 315,000 KYCed users, and over 1.1 million connected wallets. That puts DAO Maker in a different category from smaller launchpads that depend on one or two active sales to look relevant.

DAO Maker is not only a token-sale page. Its real product is structured access. Users connect a wallet, complete platform requirements, stake DAO when needed, and use launchpad mechanics to qualify for project allocations. The investment case depends on whether that access continues to attract quality projects and enough demand for DAO staking.

DAO Maker’s launchpad model is built around allocation power rather than open free-for-all participation. The platform uses staking and eligibility mechanics so that users who commit DAO can gain better access to token sales. That creates a more controlled fundraising environment for projects and a clearer participation system for users.

The staking portal supports DAO staking across several networks, including Ethereum, BNB Smart Chain, Base, and Solana. That multi-chain approach is useful because gas costs, network familiarity, and wallet preferences can change user behavior. The more important point is that staking turns DAO from a passive token into an access instrument.

That model works best when DAO Maker has strong launch flow. If new projects are attractive, users have a reason to stake, hold, and compete for allocations. If deal flow slows, DAO utility weakens because fewer users need allocation power. This is the core tension in every launchpad token, and DAO is no exception.

DAO is the central token for the DAO Maker ecosystem. Its main role is launchpad participation and staking access. Users who want stronger participation rights generally need to hold or stake DAO, then follow sale rules around registration, KYC, allocation, and distribution.

The token utility is cleaner than many small-cap crypto assets because it has a direct platform function. DAO is not only a governance-style asset waiting for a future use case. It already connects to staking, launchpad access, and allocation mechanics.

The weakness is market demand. DAO utility is valuable only when launchpad access is valuable. If early-stage token launches underperform, if participation demand falls, or if users stop competing for allocations, the token can trade mainly as a speculative small-cap asset. That is why DAO Maker should be reviewed by both platform activity and token liquidity.

DAO’s market profile is the biggest caution in this review. At the time of review, DAO traded near $0.04, with a market cap below $10 million and daily trading volume under $1 million. That is far below the valuation profile many launchpad tokens carried during the 2021 IDO cycle.

This creates two possible readings. The bullish view is that DAO Maker still has real infrastructure, visible user metrics, and a recognizable launchpad brand while DAO trades at a small-cap valuation. The bearish view is that the market has already discounted launchpad demand, and DAO needs fresh catalysts before a stronger token recovery becomes credible.

The token’s low market cap can make upside look attractive, but it also increases volatility. Thin liquidity can amplify both rallies and selloffs. Users who buy DAO only to qualify for launches should treat the token exposure as part of the investment risk, not as a neutral ticket cost.

DAO Maker’s strongest advantage is operating history. The project has survived multiple market cycles, changed with launchpad demand, and kept its app infrastructure active. That gives it more credibility than newer launchpads with limited records.

The platform’s launchpad value comes from screening, allocation design, KYC, token distribution, and community reach. For projects, DAO Maker can offer access to a large retail audience. For participants, the platform can reduce some discovery friction by packaging early-stage opportunities inside a structured environment.

That does not remove deal risk. Early-stage tokens can fail even when the launchpad is credible. Users still need to assess project valuations, vesting schedules, token unlocks, market timing, product quality, team execution, and post-listing liquidity.

DAO Maker’s biggest strength is that it is still an active launchpad brand with real user infrastructure. The scale of connected wallets and KYCed users matters because launchpads depend on distribution.

The second strength is token utility. DAO has a direct function inside the ecosystem, especially through staking and launchpad access. That gives the token a clearer purpose than many small-cap assets.

The third strength is product breadth. Launchpad, staking, farms, vaults, and airdrop tools create more surface area than a single sale page. That can help DAO Maker remain useful even when IDO demand is uneven.

DAO Maker’s main weakness is token momentum. DAO’s price and market cap suggest the market is not treating the platform like a dominant launchpad leader in 2026. That can change, but it requires stronger launches, better demand, and renewed interest in early-stage token access.

The second risk is allocation competition. Launchpad access can require staking, KYC, registration, timing discipline, and luck. Users can hold DAO and still fail to receive the allocation they wanted.

The third risk is early-stage token quality. Launchpad participation is not the same as buying a mature asset. Sales can underperform after listing, vesting can create sell pressure, and project execution can disappoint.

DAO Maker remains one of the more credible legacy launchpads in 2026. The product is real, the platform metrics are meaningful, and DAO has clear utility through staking and launchpad access.

The investment case is more cautious. DAO trades like a small-cap recovery asset, not like a sector leader. That creates upside potential if launchpad demand returns, but it also creates high liquidity and volatility risk.

DAO Maker earns a 7.3/10 because the platform has history, user scale, and clear token utility. It does not score higher because DAO still needs stronger market momentum, higher-quality current launches, deeper liquidity, and clearer evidence that staking demand can return at scale.

DAO Maker is a serious launchpad platform with a real operating history, active staking infrastructure, and a direct role for the DAO token. It is best suited to users who want structured early-stage access and understand that launchpad investing carries high risk.

The strongest reason to use DAO Maker is not passive DAO exposure. It is the ability to participate in a platform built for early-stage crypto allocations. The biggest risk is that launchpad demand remains weaker than past cycles. Users should judge DAO Maker by current launch quality, allocation rules, token liquidity, staking demand, and post-sale performance before treating DAO as a long-term recovery play.

The post DAO Maker Review: Launchpad, DAO Token, Staking And 2026 Outlook appeared first on Crypto Adventure.