Picture this: you’re a small business owner, juggling invoices and taxes, when Intuit’s AI steps in to predict a cash crunch and automate your books-saving you hours and dollars. Now, as an investor, you can own a piece of that magic. Intuit, the $190 billion fintech titan behind TurboTax and QuickBooks, is riding an AI-fueled wave with 29% stock gains this year, outpacing the S&P 500. Here’s why its stock forecast-projecting up to $2,373 by 2029-demands your attention, whether you’re a retail dreamer or an institutional strategist.

Imagine a world where small businesses don’t just survive-they thrive, armed with tools that predict cash flow hiccups before they hit and automate tax woes with a click. That’s Intuit’s magic. As the brains behind TurboTax, QuickBooks, and Credit Karma, this $190 billion giant isn’t just software; it’s the silent engine powering 100 million users worldwide to pocket more cash and waste less time. With AI agents now handling everything from invoice chasing to personalized advice, Intuit’s turning everyday entrepreneurs into efficiency machines.

Intuit’s fiscal 2025 was a blockbuster: revenue surged 16% to $18.8 billion, driven by TurboTax’s 8% jump and Credit Karma’s explosive 32% growth. Operating margins hit a stellar 26%, with non-GAAP EPS climbing to $19.16-up 13%-proving the AI bet is paying off big. For 2026, they’re eyeing 14–15% revenue growth to $21 billion, with EPS at $23, blending steady cash flows (87% recurring) and smart cost controls into a recipe for sustained dominance.

Intuit has delivered a robust long-term average annual revenue growth rate of 16.21%, showcasing its powerhouse status. Recently, growth has tapered slightly, but the company’s AI-driven momentum keeps it firmly on an upward trajectory for investors.

Intuit’s EPS growth CAGR is even more striking, soaring to an impressive 17.17%. Over the past five years, the average annual EPS growth has been a robust 20.25%.

This rapid pace seems significantly driven by the company’s aggressive share buyback program, which has reduced outstanding shares, boosting per-share earnings while reinforcing investor confidence in sustained value creation.

Intuit’s shares have been on a tear, up 29% year-to-date to around $690 as of late September, outpacing the S&P 500’s 20% gain. The secret sauce? Q4 earnings crushed estimates (20% revenue pop), sparking a 3% after-hours rally, while a fresh $3.2 billion buyback authorization signals boardroom confidence in undervalued shares. Even with a forward P/E of 29 -premium but justified by 20% projected growth-analysts see room to climb toward $800, fueled by AI’s sticky ecosystem locking in loyal users.

The stock price has risen by more than 26 284% since the IPO.

In the cutthroat fintech fray, Intuit towers over rivals with its 60% U.S. tax software stranglehold and AI moat that’s tough to breach. H&R Block lags in innovation, Wolters Kluwer focuses on enterprise giants, while Thomson Reuters plays catch-up in small biz tools. Intuit’s secret weapon? A unified platform blending tax, payroll, and marketing-leaving competitors scrambling as it gobbles mid-market share with 19% QuickBooks growth.

Competitor Comparison Table

Intuit’s profitability metrics are so stellar they practically scream “market leader in the making.” We believe the stock, as of this writing, is fairly valued, with our price target suggesting growth could match or even outpace its historical 23%+ CAGR.

While the dividend yield lags the market average, the 15%+ annual dividend growth rate is a quiet flex of strength. Want to yell “Show me the money!”? Skip the theatrics-buy Intuit’s stock, reinvest those dividends, and scoop up more shares during dips to ride this cash-generating juggernaut to the top.

2025–2029 Price Targets:

*Theoretical calculation. Actual results may differ significantly due to market conditions as well as your investment strategy and tactics.

At the time of writing, Intuit’s stock has pulled back from its all-time high, offering a compelling entry point for investors. This dip creates an ideal window to scoop up shares or reinvest dividends, capitalizing on the company’s robust AI-driven growth and undervalued potential.

Intuit’s not hoarding cash-it’s sharing the wealth. The quarterly dividend just hiked 15% to $1.20 per share ( yield ~0.7%), paid October 17, rewarding patient holders with a 14% five-year growth streak and a rock-solid 30% payout ratio. Pair that with $2.8 billion repurchased in 2025 (total authorization now $5.3 billion), and it’s clear: management views the stock as a bargain, shrinking shares to juice EPS while AI expansions keep the growth engine humming.

September’s spotlight? Intuit’s Investor Day reaffirmed bold 20% growth targets through 2030, sending shares up 2% as analysts cheered AI’s role in TurboTax Live’s 47% surge. A Clair partnership for on-demand pay in QuickBooks? That’s instant appeal for small biz retention, potentially adding millions in ecosystem revenue. Yet, Mailchimp’s soft spot (transitory repackaging) shaved a quick 5% post-earnings- a dip-buying gift, as it underscores undervaluation amid 15% international online growth.

These wins amplify Intuit’s value: AI isn’t hype-it’s driving 19% platform revenue, fortifying the moat against free-tax threats and boosting per-user spend by 10%. For investors, it’s a green light: higher retention means fatter margins, turning one-time filers into lifelong subscribers.

Intuit’s AI-driven growth, juicy buybacks, and a dividend that keeps climbing make it a no-brainer for portfolios craving stability with a side of sizzle. With shares poised to hit $800 soon and potentially skyrocket to $2 373 by 2029, now’s the time to jump in-especially after that post-earnings dip. So, grab those shares, reinvest those dividends, and maybe wink at the skeptics still betting against this fintech juggernaut. After all, who’s laughing when your portfolio’s up 20% a year?

Or Donate:

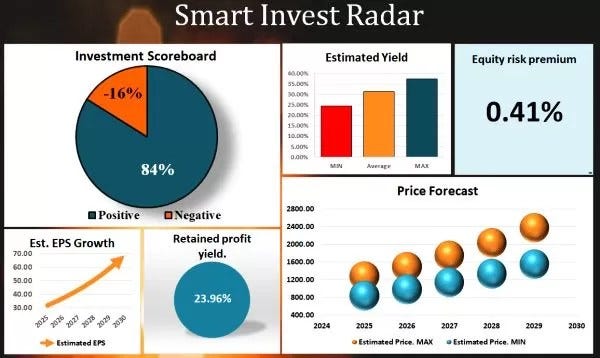

*Investment analysis involves scrutinizing over 50 different criteria to assess a company's ability to generate shareholder value. This comprehensive approach includes tracking revenue, profit, equity dynamics, dividend payments, cash flow, debt and financial management, stock price trends, bankruptcy risk, F-Score, and more. These metrics are consolidated into a straightforward Investment Scoreboard, which effectively helps predict future stock price movements.

**Use the price forecast to manage the risk of your investments.

Pažymėta: AI stocks, AI stocks for long-term investment, dividend reinvestment, fintech growth, fintech investment, fintech stocks to buy now, INTU, Intuit, Intuit AI-driven growth, Intuit dividend reinvestment strategy, Intuit share buyback program, Intuit stock, Intuit stock price forecast 2025–2029, Intuit vs H&R Block comparison, Investment, Investment Analysis, Investment Insights, QuickBooks, QuickBooks revenue growth, Share Buybacks, Stock Forecast, Stock Insights, Stock Price Forecast, Stock price prediction, Stock volatility, TurboTax, TurboTax stock investment, why invest in Intuit stock

Originally published at https://www.aipt.lt on September 24, 2025.

Is Intuit ’s Stock Your Golden Ticket to Millions? AI-Powered Gains Could Hit $2,373 by 2029! was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.