When Bitcoin was first introduced, it was presented as a peer to peer payments system without censorship. It was famously introduced just as the banking crisis was unfolding and large banks were deemed to big to fail. It was a response to a financial system that felt heavily rigged for 1% of the population.

Ethereum was the next generation of blockchain cast as the world’s computer. It enabled smart contract logic to be executed within the nodes themselves. These smart contracts enabled people to invest in ideas through “initial cryptocurrency offerings” (“ICO”) as well as extend banking services to areas without banks.

Blockchain was described as something that could bank the unbanked. It was often sold as democratising finance. It provided the means for instant settlement of transactions across borders through the removal of intermediaries and a low cost transfer.

A lot of posts and articles I have read lately suggest that privacy is the last problem to be solved before mainstream adoption; I’m going to take a different approach, knowing that it may be unpopular, and suggest that mainstream adoption will require much lower fees.

As someone who is building infrastructure on Ethereum, I can tell you that the gas consumption is only going to increase which will drive up fees. For post-quantum enabled account abstraction, the gas required to verify a signature is in the millions of units. As companies introduce privacy features, whether through zero knowledge proofs or homomorphic encryption, those features will also be gas heavy.

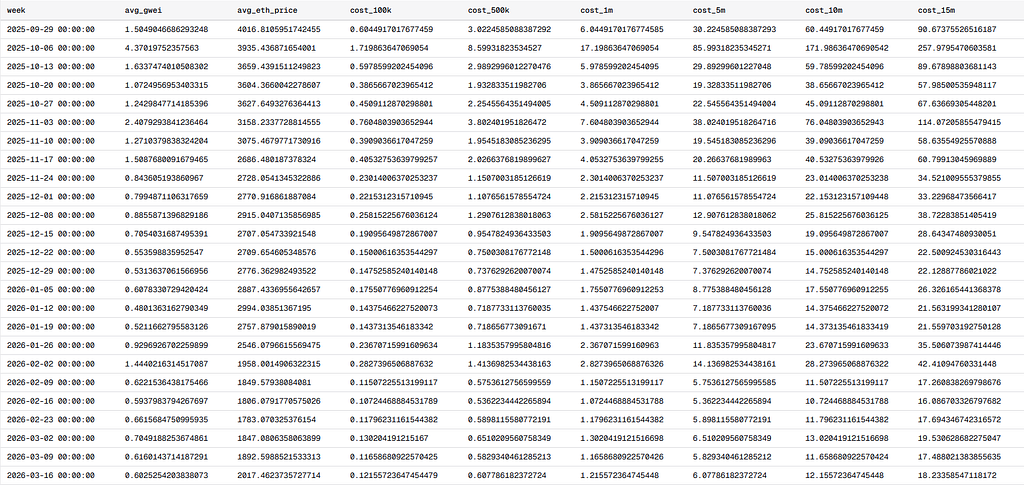

Table 1 shows the cost, in US dollars, of transactions consuming between 100,000 and 15,000,000 units of gas. This table spans from last September, when the price of ether was still near its all time high, until recently during the current bear market. You can also see that the average gas fees (avg_gwei) have also dropped considerably in that time.

The gas consumed verifying post-quantum signatures is not going to drop significantly unless a newer, leaner algorithm is discovered. Pre-compiles could be used to reduce the gas consumption but that is highly unlikely. Pre-compiles require soft forks which makes them disruptive. Creating a pre-compile would also require choosing a cryptographic algorithm and committing to it. Smart contracts give more flexibility in selecting which algorithms to use and allow for better crypto agility.

If a private and/or post-quantum transaction is going to cost multiple dollars instead of pennies, why would anyone stop using the banks and card payments? Those fees are commonly hidden (by being charged to vendors instead of consumers) and in the range of 2–3%. If it costs even $2 to send a stablecoin payment, no one will use them to buy a cup of coffee.

If blockchain want to challenge the current bank-run system, it needs to be tailored to the needs of the other 99%. Otherwise it is in danger of becoming the very system it was intended to replace; one designed for a select few successful people.

I know people will say this is what layer two chains are for, they have significantly lower costs. Layer two chains are not decentralised enough as highlighted by Vitalik earlier this year. Their validators are more like stewards managing a system in the hope that they grow enough to become decentralised. The lack of decentralisation in these chains means that they can still be subject to censorship, state intervention, and weaker security controls.

During the NFT craze, the gas fees were extremely high. Transactions that previously cost pennies were suddenly costing dollars. Even transferring bitcoin cost more than a few dollars. Gas fees increase during times of high congestion but that just enables those with means to continue to benefit from the system while everyone else watches from the sidelines. How can that make a good user experience?

Blockchains today feel less accessible and more about extracting value. It is a new financial system where some early adopters, some of whom came across it via Silk Road to feed drug habits, are heavily rewarded for being at the right place at the right time and not because they added value.

There is less talk about providing banking services to the world. In the industry, the hottest topic at the moment is yield bearing stable coins. Someone who holds a few hundred stable coins is not going to significantly benefit from yield. Yield farming was only ever lucrative to those with very large balances to begin with; anyone staking less than a thousand dollars would be lucky to earn even a few dollars.

The industry has lost its way, in fact. The promise was a new financial system with fiduciary freedom but it is instead turning into a system that increasingly favours capital-rich users, institutions, insiders, and speculators. The average person is being priced out of participation through higher fees, liquidity requirements, and speculative value extraction.

Anyone who has not already benefited from the technology may feel that they have already missed the opportunity. The fact that the ecosystem is still rife with scams and insider fraud does not help. But to be told that this is the future but still be expected to pay high fees is just crazy. Where is the benefit for the average user? The only apparent benefits are the operational efficiencies and fast settlement times but these present more of a benefit to the companies offering financial services rather than the end user.

For this technology to become mainstream, it needs a much higher adoption rate. Getting more people to use the technology is beneficial for blockchain since that increases the number of independent nodes on the network further increasing decentralisation.

How can we do this, you may ask? The network needs to scale immensely and sharding could do that. The network needs to be flooded with a lot more transactions at a significantly lower price. The goal should be low fees similar to Hedera where most transactions cost one tenth of a penny.

Sharding, if done right, can increase the number of transactions without increasing the workload of validators at scale.

If the community was ever serious about the democratisation of finance, then they need to reflect on the current situation before ordinary people are priced out of participation.

Mainstream Adoption Requires Lower Fees was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.